Best Cash Back Credit Cards in Canada for 2026

Simplified rewards for everyday Canadians

It's a competitive category, but the best cash back credit card is the MBNA Rewards World Elite Mastercard. It has the highest average rate of return for a reasonable annual fee and even offers bonus points on your birthday.

×7 Award winner

×7 Award winner

7x Award winner

7x Award winner

This article reviews the best cash back card options by category, so you can maximize the cash back you earn based on your actual spending habits. We've provided all the details you need to choose the right card for your lifestyle and budget, using data-driven analysis to rank Canadian cash back credit cards across rewards, insurance, and more.

Our listings are not limited to pure cash back cards – cards that offer reward points are also eligible. To qualify, a card simply has to offer a way to earn you cash, whether through statement credit or direct deposit (gift cards do not count).

Key Takeaways

- The best cash back credit card in Canada is the MBNA Rewards World Elite Mastercard

- Other top cash back cards include the Neo Financial World Elite Mastercard, Simplycash Preferred From American Express, Scotiabank Momentum Visa Infinite, and Rogers Red World Elite Mastercard.

- For maximum rewards, find a cash back credit card where the highest-earning categories match your spending habits.

- Some cards allow you to redeem your cash back whenever you like, but some automatically cash you out at specific times, or they may enforce a minimum cashout value.

The best cash back credit cards in Canada

Our Gold award for the #1 best cash back card in Canada goes to the MBNA Rewards World Elite Mastercard, thanks to its average cash back earn rate of 2.37% and bonus points on your birthday. The MBNA Rewards program offers several very valuable redemption options.

Our Silver award goes to the Neo World Elite Mastercard - Gas & Grocery, with an impressive 2.55% average earn rate and solid insurance package.

And our Bronze award goes to the SimplyCash Preferred Card from American Express, a cash back juggernaut from Amex that earns an average of 2.55% cash back and automatically pays it out every September. It's lucrative and reliable.

| Credit card | Average rate of return | Annual fee | Current welcome offer | |

|---|---|---|---|---|

| #1 | MBNA Rewards World Elite Mastercard | 2.37% | $120 |  $40 GeniusCash + 30,000 bonus points (terms) $40 GeniusCash + 30,000 bonus points (terms) |

| #2 | Neo World Elite Mastercard - Gas & Grocery | 2.55% | $149 | None |

| #3 | SimplyCash Preferred Card from American Express | 2.55% | $119.88 | 10% cash back for the first 3 months + $50 (terms) |

However, there are several other noteworthy cash back cards for all income levels and spending habits. For example, the Scotia Momentum Visa Infinite+ Card offers 11 types of insurance while still earning 2.08% on average. Similarly, the Rogers Red World Elite Mastercard shines with its lack of an annual fee and straightforward 1.5% earn rate.

#1 Best cash back credit card: MBNA Rewards World Elite® Mastercard®

×7 Award winner 7x Award winner

The MBNA Rewards World Elite Mastercard is not only the best cash back card, but it's also one of the best rewards cards, the best travel credit cards, and the best overall Mastercards in Canada – its flexibility is probably its biggest strength. And its wicked 2.37% cash back earn rate, of course.

Note that this is slightly lower than its overall earn rate of 2.86%. This card earns even more when you redeem rewards for travel.

Speaking of flexibility, MBNA Rewards can be redeemed for cash back that's deposited into your bank account, statement credits, valuable e-gift cards, or even charitable donations. All options provide high value, which is another example of its flexible nature.

Throw in World Elite Mastercard perks – like concierge services, exclusive event tickets, and airport lounge access – and you've got a winning cash back card.

[Cardholder quote from expert or team member]

Best cash back card silver winner: Neo World Elite® Mastercard - Gas & Grocery

As the silver-winning best cash back credit card, the Neo World Elite Mastercard - Gas & Grocery has some eye-popping cash back rates. For example, the base rate of 5% on groceries is fantastic. Just remember this category is capped at $1,000 in monthly spending.

Cardholders can easily outpace the reasonable $149 annual fee with consistent spending. Plus, the insurance package is very generous, with 12 types, including everything from purchase protection to rental car theft and damage.

The bronze-winning cash back card: SimplyCash® Preferred Card from American Express

The SimplyCash Preferred Card from American Express is the bronze-winning best cash back credit card and has two earn categories, each with a flat rate: 4% back on gas and groceries, 2% on everything else. Plus, your cashback is automatically paid out as a statement credit every year in September, like clockwork, with no effort on your part. It's rare to find such good rates in such an easy-to-use and easy-to-understand format.

This card is also fairly easy to apply for and be approved for, thanks to the lack of income requirements. You'll still need a good credit score, but the barrier to entry is still lower than most.

With typical Amex benefits – think Amex Offers, Amex Front of the Line, Amex purchase protection, etc. – ample insurance, and no income requirements, and a reasonable annual fee, it becomes obvious why the SimplyCash Preferred Card from American Express earns the bronze title in the best cash back card category.

The best Visa cash back card: Scotia Momentum® Visa Infinite+* Card

×2 Award winner

2x Award winner

2x Award winner The cards on this list so far are either Amex or Mastercards, but the best Visa cash back credit card is the Scotia Momentum Visa Infinite+ Card. Plenty of other cards reward grocery purchases, but this one adds recurring bill payments to its top-earning categories, including most pre-authorized payments set to automatically withdraw on a regular basis – think gym memberships, phone bills, streaming services, utilities, and more.

The Scotia Momentum Visa Infinite+ Card also has an impressive insurance package, including 11 types of coverage. This is unusual for a non-travel card, but Visa nails it.

Plus, the accompanying Visa Infinite perks offer complimentary concierge services, exclusive access to dining events, and upgrades at properties in the Visa Infinite Hotel Collection.

The best cash back card with no annual fee: Rogers Red World Elite® Mastercard

The Rogers Red World Elite Mastercard is the best cash back credit card with no annual fee – and is exactly what a flat-rate cash back credit card should be: easy to use, easy to understand, and easy to earn rewards with. Users earn 2% cash back on all eligible purchases if they have one qualifying service with Rogers, Fido, Comwave, or Shaw, and 1.5% on other eligible purchases. Plus, U.S. dollar purchases earn 3% cash back.

And all of this cash back is unlimited – no monthly or annual caps whatsoever.

Tack on a superb insurance package and World Elite Mastercard benefits, and you see why the Rogers Red World Elite Mastercard earns its spot on our list.

How the Genius Rating ranks top cash back cards

Our Genius Rating system uses a refined, math-based algorithm to generate a score out of 5 for all

How we found Canada's best cash back cards

To identify the best cash back cards in Canada, we examined over 126 credit card features in 7 main categories:

- Rewards: 54%

- Fees: 13%

- Perks: 11%

- Insurance: 11%

- Interest: 5%

- Approval: 3%

- Acceptance: 3%

Since we're talking about cash back credit cards, we gave the rewards category the most weight. Our algorithm calculated and scored every entry on this list, using a typical $3,000 monthly budget.

Learn more about our Genius Rating methodology

How to choose the right cash back credit card

When choosing the ideal cash back card for your needs, the first crucial step is to identify your top spending categories. If you spend heavily on travel, consider a card that prioritizes airfare, hotel, and foreign currency purchases. Or, if you stay closer to home, consider a card with high returns on gas, groceries, or recurring bills.

You should also consider the annual fee. Higher-fee cards typically offer high earn rates, enhanced insurance, and other perks that can offset the cost. On the other hand, no-fee cash back cards tend to have lower earn rates, smaller insurance packages, etc.

Here's a guide to help with choosing your own card by looking at the various features that contribute to a cash back card.

Rewards

Cash back cards are popular for their simplicity and robust earning potential. But getting the right card for you requires examining each offer, its spending categories, and its limitations.

Beyond simply looking at categories such as recurring bills, gas, groceries, restaurants, and others, you'll also need to pay attention to merchant category codes (MCCs). Individual credit card networks use MCCs to classify stores by their primary source of revenue, so these MCCs determine how all your purchases are categorized and how many rewards you earn.

For example, let's say you earn 4% cash back on groceries with the BMO CashBack World Elite Mastercard. Most people think of Costco as a grocery store, but because it also sells electronics, furniture, pet food, vitamins, and more, it actually falls under general merchandise – meaning you only get 1% back on what you spend in-warehouse.

Here's a look at our top five cash back cards and their average earn rates:

Tip: No matter what credit card you use, you could be earning bonus cash back on top of your card's rewards. Input your monthly spend in the GeniusCash app, and level up to earn real cash.

Approval

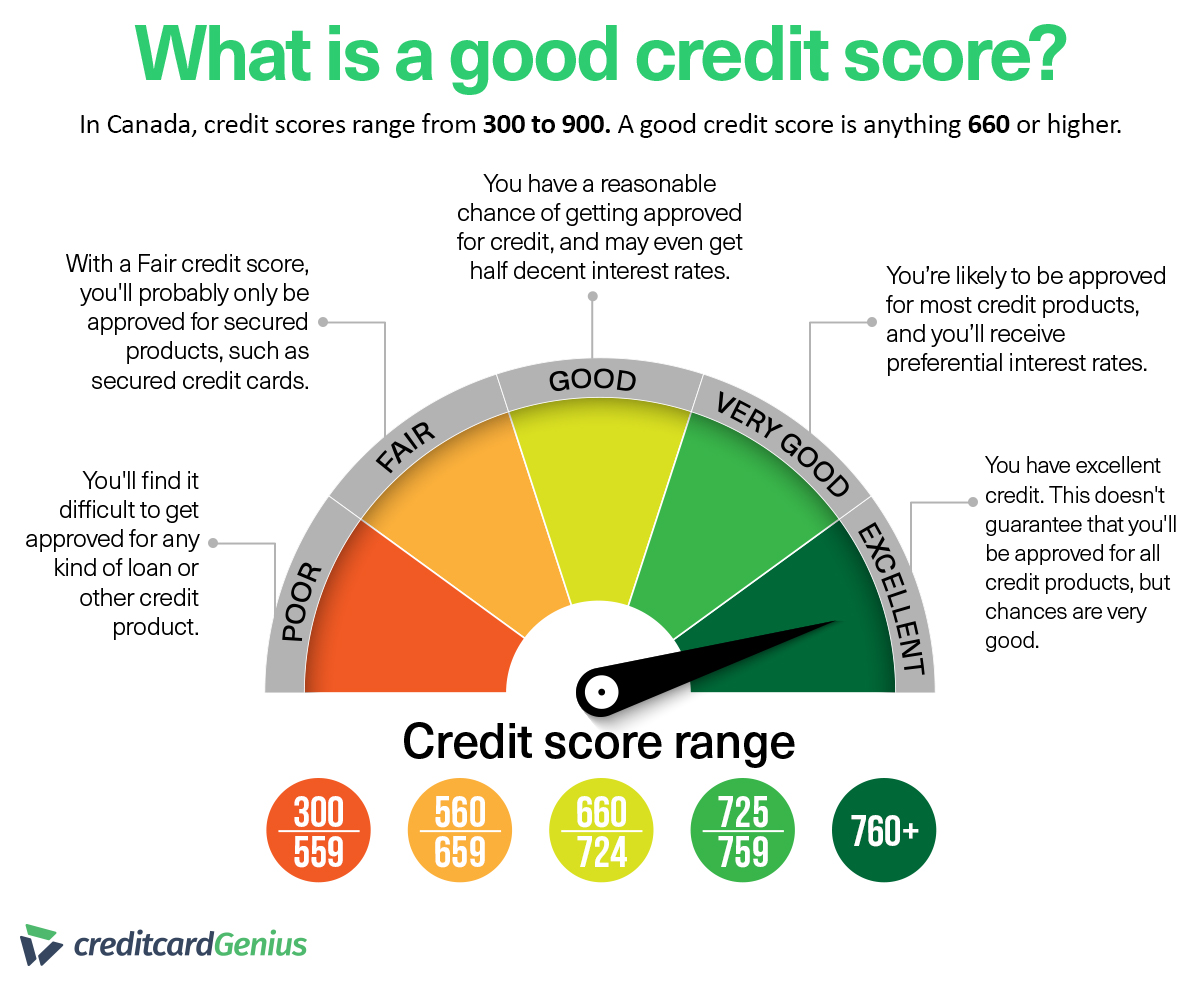

Most cash-back cards require a "good" credit score (660–724), while premium cards often look for a "very good" or "excellent" score (720+), since they offer higher rewards and additional perks. Income requirements vary, but typically range from no income verification required to around $80,000 for cards with an annual fee of $100+.

The MBNA Rewards World Elite Mastercard and Neo World Elite Mastercard - Gas & Grocery, for example, require a minimum income of either $80,000 personal or $150,000 household, while American Express has no minimum income requirements for its SimplyCash Preferred Card from American Express.

Perks

Cash back credit cards tend to offer fewer perks than other types of rewards cards, especially travel cards. Because they usually have lower annual fees than travel cards (the high for cash back cards is around $120, versus $300 for a travel card), cash back cards provide more everyday perks, like:

- Credits for streaming services or other services

- Complimentary subscriptions to food delivery apps

- Fuel discounts

Both the MBNA Rewards World Elite Mastercard and SimplyCash Preferred Card from American Express come with a unique perk: ongoing promotional financing. Amex offers something called Plan It, which lets cardholders split a large purchase into monthly installments, saving them money on interest. Similarly, MBNA offers the MBNA Payment Plan, which allows cardholders to pay off eligible purchases of $100+ over 6-, 12-, or 18-month terms.

Insurance

The insurance coverage and value you can expect from a cash back card depend on the annual fee you pay. No-fee options usually only provide basic coverage for things like:

- Extended warranty: Extends the manufacturer's warranty for up to two years, depending on the card.

- Fraud liability: Protects the cardholder from unauthorized or fraudulent purchases.

However, premium cash-back cards can offer the same extensive insurance coverage as a leading travel card, including various types like emergency medical and travel accident insurance.

This table lays out how the top five cash back cards still offer valuable travel insurance packages:

| Coverage type | MBNA Rewards World Elite Mastercard | Neo World Elite Mastercard - Gas & Grocery | SimplyCash Preferred Card from American Express | Scotia Momentum Visa Infinite+ Card | Rogers Red World Elite Mastercard |

|---|---|---|---|---|---|

| Trip interruption | $2,000 | $1,000 | N/A | $2,000 | $1,000 |

| Baggage delay | $500 | $1,000 | $500 | $500 | N/A |

| Flight delay | $500 | $500 | $500 | $500 | N/A |

| Emergency medical | N/A | 14 days | 15 days | 15 days | 10 days |

| Travel accident | $1 million | N/A | $100,000 | $500,000 | N/A |

Interest rates

Cash back cards generally have interest rates similar to other rewards cards, but they occasionally offer promotional 0% or reduced-rate offers on new purchases or balance transfers.

Typical purchase rates range from 20.99% to 21.99% for purchases (and balance transfers, where offered), and from 22.99% to 29.99% for cash advances.

Here's a look at the rates for our top five cash back cards – note that the SimplyCash Preferred Card from American Express doesn't offer balance transfers and therefore has no associated interest rate:

What is a cash back credit card?

Cash back credit cards are a type of rewards card that puts cash back in your pocket with every purchase.

The value of what you earn – also known as your rate of return – is expressed as a percentage: 2% means you get $2 back for every $100 you spend, 3% equals $3, and so on.

Value of credit card rewards / amount of money spent = rate of return

Types of cash back credit cards

There are generally three types of cash back cards: flat-rate cards, bonus-category cards, and flexible-category cards. They vary in terms of how you earn cash back.

- Flat-rate cash back cards: These earn a flat rate on purchases, regardless of spending category. These credit cards typically offer low interest rates but have no or low annual fees.

- Bonus-category cash back cards: These cards offer higher returns on specific purchase categories. Many cards place limits on how much you can earn.

- Flexible category cash-back cards: These let you choose or adjust which categories offer the best return, so your rewards are tailored to your spending habits, even as they change.

Many savvy credit card users carry multiple cards in their wallets, usually including at least one of these cash back card types.

For instance, if you have a travel credit card that earns excellent returns on flights but little to nothing on gas or groceries, consider a bonus-category card with a high return rate for your weekly shopping trips – the MBNA Rewards World Elite Mastercard, for instance.

Earn extra cash back with GeniusCash

No matter which credit card you decide to use, you can use the GeniusCash app to earn bonus cash back on top of what your card offers.

GeniusCash is a Canadian rewards program that offers cash back as Interac e-Transfers or PayPal payments. While GeniusCash is known for offering payouts when you open a new banking product, you can also earn GeniusCash on a monthly basis by taking advantage of the Max feature.

Max allows you to earn cash back based on the level you've achieved in the GeniusCash app.

How GeniusCash Max works

The first step is adding your credit cards to your Max wallet. You don't need to input any actual credit card information. You just need to select the cards you use and input your spending for each card.

When you break your spending down into categories, Max analyzes your habits and offers suggestions to earn more rewards. For example, Max will tell you when you're missing out on points by using one card over another. Max can even suggest new credit cards that could earn more rewards.

Each month, you can also earn up to 1% cash back on your spending, up to a monthly cap. With your first level, you'll start earning 0.1% on every dollar, and you can increase this amount by another 0.1% every time you level up – all the way to level 10.

Tips for maximizing cash back

If you're a spend-and-forget-about-it kind of consumer, you might be missing out on valuable cash back rewards. To ensure you're squeezing the most value from your card, try strategies like adding authorized users and taking advantage of bonus offers:

Here's a list of our top tips for maximizing your cash back potential:

- Use a card that matches your spending habits: Track your spending for a few months to see where you spend the most. Then choose a card that offers high returns in your top spending category or categories. This way, you'll boost cash back without adjusting your shopping habits.

- Watch for bonus rewards offers: Issuers occasionally run credit card promotions to encourage people to spend more, shop with specific partners, etc. You might see these offers when you log into your account, or you might receive a promotional email.

- Hit the spending requirements for bonuses: If your card offers a cash-back welcome bonus, read the fine print to see how much you need to spend within a specific period. For instance, you might have to spend $3,000 within the first six months to earn a $300 welcome bonus.

- Add authorized users: Not every issuer allows this, but if you can, add authorized users and supplementary cards. Their purchases will earn rewards for your account. Be sure to check whether your card charges extra fees for additional cards, though.

- Keep your cards paid off: If you're carrying a balance from month to month, you're losing money – your rewards won't offset the interest you're charged.

Cash back earning caps

Earning caps are an often-overlooked condition of credit card spending. Although some credit cards don't put a limit on the rewards you can earn, some do, and cap your rewards once you reach a specific spending threshold.

For example, if your card earns 5 points per $1 on groceries up to $15,000 in spending, you'll earn the extra points on that $15,000. After that, all other grocery purchases only earn the base spending rate.

Some credit cards have low spending caps, so it's important to pay attention to these terms when comparing credit card earn rates.

How to redeem cash back rewards

Some companies put you in control of deciding how and when to cash in your rewards, while others only let you redeem at specific intervals. If your credit card issuer offers cash back on demand, you can request your cash back through your online account.

Annual cash back usually takes the form of a bank deposit, statement credit, or (as in the case of the CIBC Costco Mastercard) a rebate coupon you use at a specific retailer. If you're using a rewards credit card, you have other options too, including charitable donations, gift cards, or statement credits.

You can usually track how much cash back you've earned by logging into your online banking account or your bank's mobile app.

Before you cash out your rewards, check your terms and conditions to see if there are minimum reward requirements. For instance, some cards require you to earn at least $10 in cash back before you can redeem the rewards.

When can you redeem your cash back?

It's crucial to understand whether your card automatically applies cash back to statements (typically either every statement cycle or annually, on the card's anniversary) or if you need to initiate the cash back payout manually.

To help you keep track of when you can enjoy your hard-earned rewards, take a look at the chart below:

| Card issuer | Credit card | When you can redeem |

|---|---|---|

| American Express | American Express Cobalt Card | Whenever you like, as long as you redeem a minimum of $10 |

| SimplyCash Preferred Card from American Express | Statement credit issued once per year in September | |

| BMO | BMO CashBack World Elite Mastercard | Whenever you like, as long as you redeem a minimum of $25 |

| BMO eclipse Visa Infinite Card | Points credited to your statement once per month | |

| CIBC | CIBC Dividend Visa Infinite Card | Whenever you like, as long as you redeem a minimum of $25 |

| Home Trust | Home Trust Preferred Visa | Statement credit issued once per year in January |

| MBNA | MBNA Rewards World Elite Mastercard | Whenever you like |

| Neo | Neo World Elite Mastercard - Gas & Grocery | Whenever you like |

| Rogers | Rogers Red World Elite Mastercard | Whenever you like, as long as you redeem a minimum of $10 |

| Scotiabank | Scotia Momentum Visa Infinite+ Card | Whenever you like, as long as you have at least $25 accumulated |

| Tangerine | Tangerine Money-Back Credit Card | Rewards paid once per month |

| TD | TD Cash Back Visa Infinite Card | Whenever you like, as long as you have at least $1 accumulated |

Pros and cons of cash back credit cards

Perhaps the best benefit of cash back credit cards is the simplicity of them, but this can come at a cost – points and travel cards often provide higher earning potential.

Here's a look at the main pros and cons of cash back cards:

Pros of cash back credit cards

- Simple, easy rewards: Cash back is straightforward and easy to manage. There's no need to convert point values to dollars, look for the highest-value redemption option, etc. Just cash out and enjoy.

- Flexible redemption: Unlike travel points, cash back can be applied to anything, whether it's groceries, bills, a night out, or whatever you like – and it can be used for something completely different next time.

- No expiration dates (usually): Most cash back cards let your rewards accumulate indefinitely, with none of the use-it-or-lose-it pressure that some travel points programs have.

- Variety of types: There's a cash back card for nearly every credit profile and spending pattern, from no-fee to premium.

Cons of cash back credit cards

- Not the highest-value option: Especially if you enjoy travelling, loyalty and travel rewards cards can stretch your spending further, sometimes significantly so.

- Earn rates vary by category: Flat rate cash back cards are rare, so you won't earn the most on all your spending. Categories often have caps too, limiting rewards on your spending even more.

- Redemption minimums: Many cash back cards require you to bank a minimum amount of cash back before you can cash out (as noted above). It may be as low as $1, but it's still an annoying detail to have to remember.

FAQ

Which credit card is best in Canada for cash back?

The best cash back credit card in Canada is the MBNA Rewards World Elite Mastercard. It's incredible 2.37% cash back earn rate is what puts it on top, but the flexibility of the MBNA Rewards program, the included 12 types of insurance coverage, and generous World Elite perks add to its value.

What card has 5% cash back?

Right now, the BMO CashBack World Elite Mastercard and Neo World Elite Mastercard - Gas & Grocery both offer 5% cash back on grocery purchass, with the BMO capping rewards at $500 and the Neo card at $1,000 per month. The Neo card also has various partner offers with an average value of 5% cash back.

What is the best credit card with the most cash back?

While technically a rewards card, the overall best cash back credit card is the MBNA Rewards World Elite Mastercard, thanks to the flexibility of MBNA Rewards and its premium World Elite Mastercard perks. The Neo World Elite Mastercard - Gas & Grocery and SimplyCash Preferred Card from American Express are also strong contenders, offering cash back rates up to 5% and 4%, respectively.

What are the downsides of cashback cards?

The main downside of cash back cards is limited flexibility – your rewards are typically redeemable only as statement credits or deposits, unlike reward points that can be transferred or used for travel. High annual fees and income requirements can also eat into your earnings, and some cards cap how much cash back you can earn in certain categories.

Is a 2% cash back card worth it?

A 2% return rate is average, but it can still be worth it if the rest of the card's features and details align with your goals. You'll want to make sure you earn enough cash back to cover the annual fee and check whether there are any caps on spending categories.

What are common bonus categories for a cash back card?

Groceries, dining, gas, and transit are some of the most common and valuable cash back categories, though the earn rates vary significantly between cards. Transit, recurring bills, travel, and streaming services categories are also very popular. The best cash back cards offer a combination of several of these categories.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.