Best No-Fee Cash Back Credit Cards in Canada for 2026

Get rewarded for free. Simple as that.

The Rogers Red World Elite Mastercard is the best no-fee cash back credit card in Canada, thanks to its excellent earn rates. The SimplyCash Card from American Express and Tangerine Money-Back Credit Card are the top runners-up.

| Credit card | Average rate of return | Current welcome offer | |

|---|---|---|---|

| #1 | Rogers Red World Elite Mastercard | 1.5% | None |

| #2 | SimplyCash Card from American Express | 1.46% | 5% cash back for the first 3 months (terms) |

| #3 | Tangerine Money-Back Credit Card | 1.14% |  $75 GeniusCash + 10% extra cash back for the first 2 months (terms) $75 GeniusCash + 10% extra cash back for the first 2 months (terms) |

These credit cards offer users the opportunity to earn cash back at competitive rates while still saving on that annoying annual fee. When comparing these cards with their fee-driven counterparts, the perks may not be quite as impressive, but the insurance coverage and other benefits are still significant.

You'll find detailed reviews below of Canada's top no-fee cash back cards, with all the information you need to feel confident in your card choices.

Key Takeaways

- The best no-fee cash back credit card in Canada is the Rogers Red World Elite Mastercard.

- Choose a card that offers high rates for the categories where you spend the most money.

- Most no-fee credit cards offer some rewards and perks, though typically not as much as more premium cards with annual fees.

- If you charge a lot to your credit card each month, it’s probably time to consider upgrading to a card that will earn you more rewards and include extra perks and benefits.

The best no-fee cash back credit cards in Canada

Our Gold award for the #1 no-fee cash back card in Canada goes to the Rogers Red World Elite Mastercard. This is mostly thanks to its 1.5% average earn rate, but it has many other rewarding features.

Our Silver award goes to the SimplyCash Card from American Express for its convenient – and valuable – flat-rate earn rates, plus it's generous welcome offer.

And our Bronze award goes to the Tangerine Money-Back Credit Card, a unique card that allows you to choose your own two, possibly three, cash back categories.

Canada's best no-fee cash back card: Rogers Red World Elite® Mastercard

The Rogers Red World Elite® Mastercard offers an impressive 3% cash back on U.S. dollar purchases, making it a worthwhile option if you frequently travel to the U.S. or make purchases on American websites Users also get an extra 2% back on all other purchases if they have qualifying Rogers, Fido, Shaw, or Comwave services. These customers also get five times more cash back when redeeming for Rogers, Fido or Shaw purchases.

But don't worry, even if you don’t have a Rogers service, you’ll still earn a flat 1.5% back on all other purchases, which is pretty considerable.

Really, this card is a Rogers customer's best friend, especially if they travel. They’ll receive five complimentary Roam Like Home days each year, providing mobile data when they're outside their coverage area. Add robust insurance – 6 types – and you have a versatile card without an annual fee.

Silver award no-fee cash back credit card: SimplyCash® Card from American Express

×1 Award winner

×1 Award winner Earn 5% cash back on all purchases in first 3 months - up to $100 in cash back.

1x Award winner

1x Award winner Earn 5% cash back on all purchases in first 3 months - up to $100 in cash back.

The SimplyCash® Card from American Express stands out for its lucrative welcome offer of 5% cash back for the first 3 months (terms), which is valued at up to $2,000. Beyond this, this card earns 2% back on gas and groceries, and 1.25% back on all other purchases. This calculates to a solid 1.46% average earn rate.

American Express provides several exclusive programs and benefits for its cardholders, including savings via Amex Offers, installment plans through Amex Plan It, and special access to events with American Express Front of the Line. All of these add significantly to the SimplyCash Card from American Express's overall value.

This card doesn't have any income requirements, which makes it a bit easier to qualify for. It also doesn't charge fees for additional cards, so the whole family can help you earn that sweet cash back.

Bronze award no-fee cash back credit card: Tangerine Money-Back Credit Card

×2 Award winner

2x Award winner

2x Award winner

The Tangerine Money-Back Credit Card is a surprising type of cash back card that puts the freedom of choice in your wallet. You'll earn 2% back in up to three categories you choose (the third pick is unlocked when you deposit your rewards into a Tangerine Savings Account), with 12 categories to choose from, including dining, groceries, gas, bills, and transit. You can change your preferred categories whenever you like, though it does take about 90 days for the change to take effect.

Having your choice of cash back categories isn't the only convenient feature – your cash back is paid out every month. You can choose to either have it applied as a statement credit or deposited into your Tangerine Savings Account.

The Tangerine Money-Back Credit Card also has a valuable promo for balance transfers. You can get a 1.95% rate for 6 months, with a reasonable 1% transfer fee.

Compare all no-fee cash back credit cards by Genius Rating

Our Genius Rating system uses a refined, math-based algorithm to evaluate each of the

Here’s how the top no-fee cash back cards compare when arranged by Genius Rating:

×1 Award winner Earn 5% cash back on all purchases in first 3 months - up to $100 in cash back.

1x Award winner Earn 5% cash back on all purchases in first 3 months - up to $100 in cash back.

×2 Award winner 2x Award winner

×1 Award winner

×1 Award winner

1x Award winner

1x Award winner The Genius Rating methodology

To determine the best no-fee cash back credit cards, we evaluate more than 126 card features across seven main categories. And since we're discussing no-fee credit cards, we give extra weight to both the fees and rewards categories – they're the primary features we're after with cards on this page.

Here's the breakdown:

- Rewards: 38%

- Fees: 38%

- Insurance: 8%

- Perks: 8%

- Interest: 8%

- Approval: 2%

- Acceptance: 2%

Learn more about our Genius Rating methodology

How to choose the right no-fee cash back credit card

There are quite a few no-fee credit cards, and choosing the right one requires considering the features and fees. Carefully examine each card’s rewards categories to find the option that best fits your needs (whether travel, everyday savings, or paying your bills). Additionally, consider the interest rates if you plan to carry a balance.

Rewards

Cash back is the most popular rewards type because it offers simplicity. Instead of worrying about things like point transfers and maximizing the value of airline miles, cash back lets you earn rewards quickly with everyday purchases.

Of course, you'll need to look at which spending categories earn the most cash back with each card you're considering. For example, if the highest cash back rate is for gas purchases, but you cycle to work and want a card that rewards grocery shopping, this card might not be of much benefit to you.

Here's how the average earn rates of the top three no-fee cash back cards compare:

Tip: No matter what credit card you use, you could be earning bonus cash back on top of your card's rewards. Input your monthly spend in the GeniusCash app, and level up to earn real cash.

Fees

Typically, the higher a card's annual fee, the more valuable and exclusive its perks and benefits are. This doesn't mean that no-fee cards don't offer competitive features, but they're usually not as premium as those of higher-fee cards.

Since we're looking at no-fee cash back cards here, you won't have to worry about the annual fee at all. There are still several other fees to consider, though, including these:

- Foreign transaction fees

- Supplemental card fees

- Overlimit fees

- Late payment fees

Insurance

No-fee cash back cards typically offer only the most basic insurance, such as zero fraud liability, extended warranty, and purchase protection.

However, just because a card doesn’t charge an annual fee doesn’t mean you can’t get decent insurance value. The Rogers Red World Elite Mastercard, for instance, provides 6 types of insurance, for a total value of about $414.

Take a look at the insurance value of the top three no-fee cash back cards:

Perks

Perks are somewhat limited with no-fee cash back credit cards. They're usually related to fuel discounts or in-store savings with eligible brands.

There are, of course, some exceptions. The SimplyCash® Card from American Express gives access to a slew of exclusive Amex programs, and the Tangerine Money-Back Credit Card allows you to choose your cash back categories – which isn't usually considered a perk, but it's so rare that we're including it.

Aside from its boosted cash back rates for Rogers, Fido, Shaw, and Comwave clients, the Rogers Red World Elite Mastercard also provides five "Roam Like Home" days of mobile data at no cost with an eligible Rogers mobile plan. Cardholders also have access to the World Elite Mastercard program, which offers many perks and benefits, like complimentary concierge service and sweet travel upgrades through Mastercard World Experiences.

When should you upgrade your no-fee card?

There are times when upgrading from a no-fee credit card to one with an annual fee can be beneficial, particularly if your spending has significantly increased or your lifestyle has changed. For instance, if you find that you're travelling more than you used to, upgrading to a travel card with a valuable rewards program could be very beneficial.

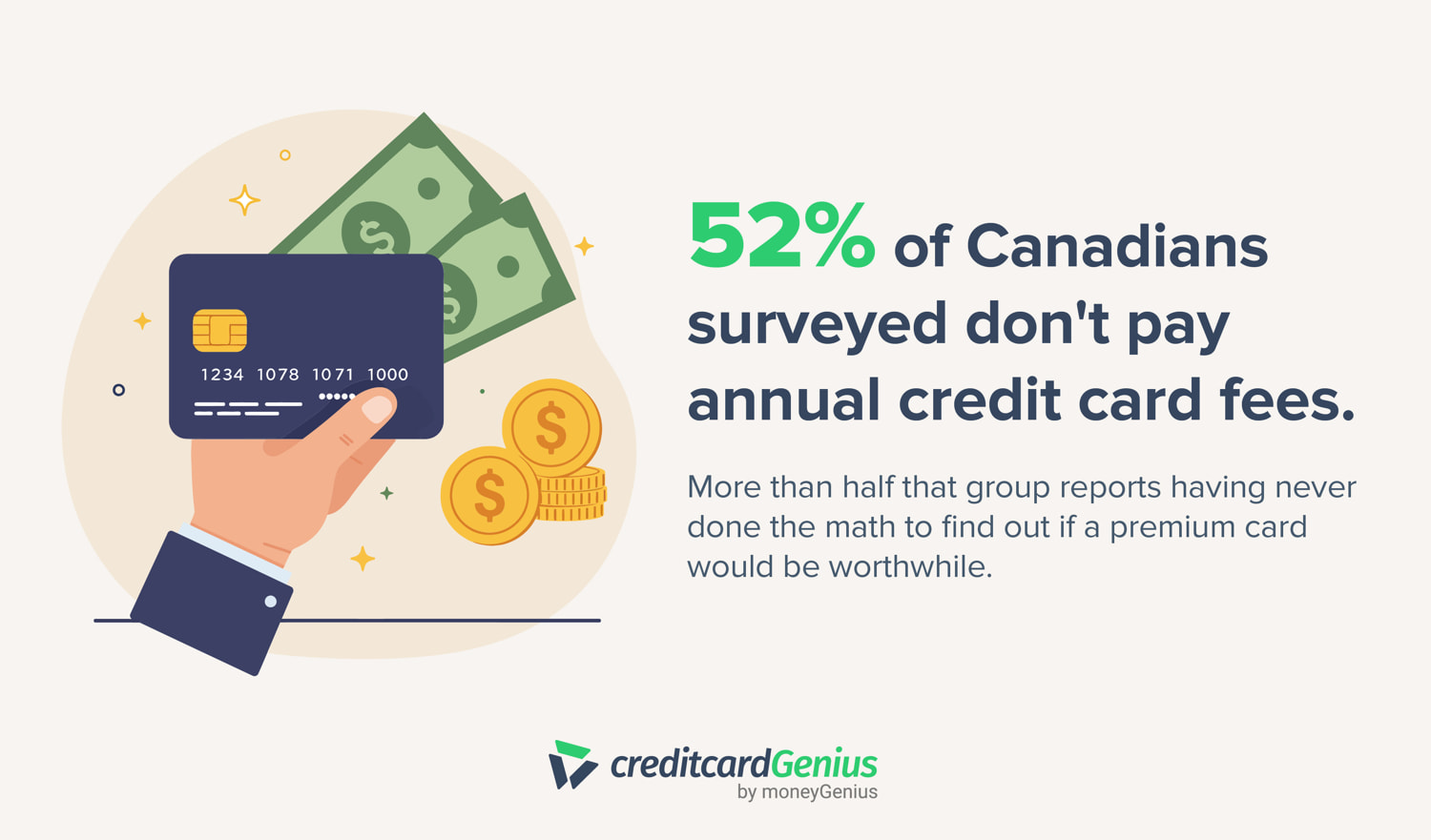

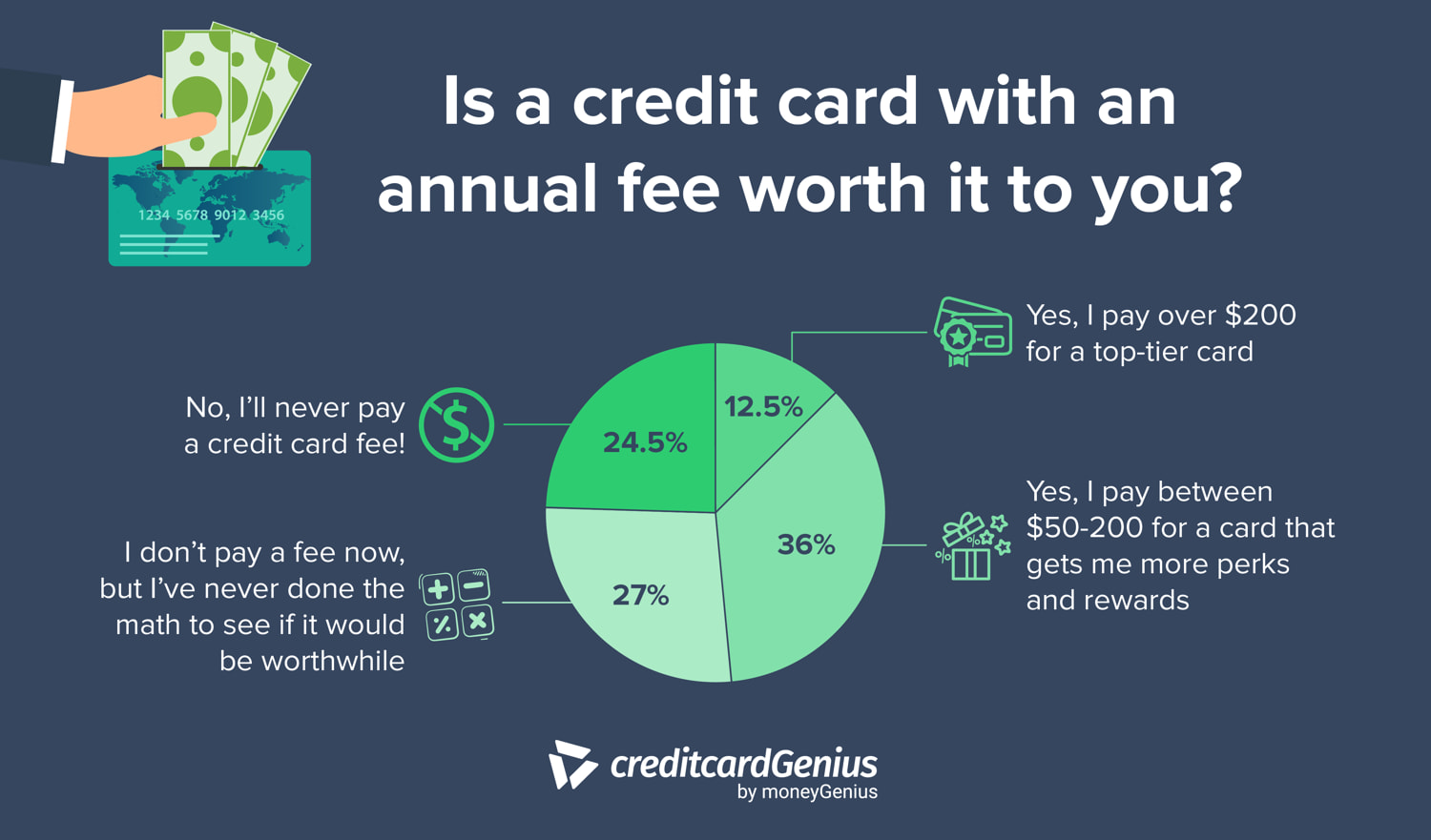

We surveyed Canadians about annual credit card fees and found that 52% don't pay for credit cards. But just over half of that group has never actually calculated whether paying for a card could actually earn enough rewards – or offer enough perks – to make the fee worthwhile.

Some cards offer free roadside assistance, and some travel cards include complimentary airport lounge visits. If you're already paying for these services in other ways, a credit card that includes them might actually help you save money, even if there is an annual fee.

To help make the decision, calculate how much you could currently earn in cash back over the course of a year. If your earned cash back is worth more than the annual fee amount of the card(s) you're considering, it's likely a good idea to upgrade.

You can download the GeniusCash app and use Max to review your spending and find suggestions for cards that out-earn your current wallet.

Many cards offer annual fee waivers for the first year, which can make the upgrade a little less daunting – and a little more valuable.

Curious what other Canadians are choosing? Our survey says 36% pay a standard fee for added perks and rewards, while 12.5% spring for an ultra-premium card.

FAQ

What is the best credit card with no annual fee and cash back?

Our top pick for the best no-fee cash back credit card is the Rogers Red World Elite® Mastercard. This card provides a flat 1.5% cash back – bumped to 2% for eligible Rogers, Fido, Comwave, and Shaw customers. USD purchases earn 3% back. You can also get extra cash back when you redeem for Rogers, Fido, and Shaw services.

What is the best no-fee credit card in Canada?

In Canada, the Rogers Red World Elite® Mastercard is the best no-fee cash back card. The More Rewards RBC Visa Infinite is the overall best no-fee travel credit card, and the Venn Corporate Card is the top no-fee card for businesses.

Which credit card gives the highest cash back?

The MBNA Rewards World Elite® Mastercard® has an incredibly high average earn rate of 2.86%. This rate includes 5 points for every dollar spent at restaurants, on groceries, and on certain recurring bills – everything else earns 1 point per dollar. Note that your “cash back” will be in the form of gift cards or e-gift cards.

Is there a downside to cash back credit cards?

Some cash back cards put caps on the amount of cash back you can earn in specific categories. There can also be restrictions on when and how you redeem your cash back – some allow you to redeem it whenever you want, while others only pay out once per year, on a certain date.

What is the annual fee for TD cash back?

There are three cash back cards available from TD: the TD Cash Back Visa Infinite Card, TD Cash Back Visa Card, and TD Business Cash Back Visa. The TD Cash Back Visa Infinite Card charges an annual fee of $139. The other cards have no annual fee.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.