Best Travel Insurance Credit Cards In Canada For 2026

Get the most comprehensive travel insurance coverage with these credit cards.

The best travel insurance credit card is the RBC Avion Visa Infinite Privilege, which offers an extensive insurance package and a range of luxurious travel perks. In addition to travel accident, trip interruption, trip cancellation, and emergency medical insurance, cardholders can also enjoy complimentary hotel upgrades, concierge services, and more.

The Scotiabank Passport Visa Infinite Privilege Card and CIBC Aeroplan Visa Infinite Privilege Card are also top travel insurance credit cards with additional perks and rewards.

| Credit card | Annual fee | Types of coverage | Est. coverage value | |

|---|---|---|---|---|

| #1 | RBC Avion Visa Infinite Privilege | $399 | 12/17 | $653 |

| #2 | Scotiabank Passport Visa Infinite Privilege Card | $599 | 12/17 | $650 |

| #3 | CIBC Aeroplan Visa Infinite Privilege Card | $599 | 12/17 | $534 |

A truly great travel insurance credit card can give you peace of mind (and save you money) with coverage for medical emergencies, rental car damage, flight or baggage delays or loss, or even hotel burglary.

While credit card insurance packages tend to centre around travel, you can also find cards with other useful insurance benefits, like purchase protection and mobile device protection.

We reviewed every credit card in Canada using our data-driven algorithm to assign each card scores across several Genius Rating categories. In this guide, you'll find in-depth reviews and comparisons of the top insurance credit cards in Canada, based on the value and variety of their insurance packages.

Key Takeaways

- The best travel insurance credit card in Canada is the RBC Avion Visa Infinite Privilege, which balances generous insurance coverage with high-value rewards.

- The Scotiabank Passport Visa Infinite Privilege Card waives FX fees, making it an excellent international shopping card.

- The CIBC Aeroplan Visa Infinite Privilege Card offers the best return rate on travel, especially if you travel via Air Canada.

- Travel insurance credit cards provide peace of mind at the cost of increased annual fees and income requirements.

- The National Bank World Elite Mastercard offers strong insurance for a lower annual fee of $150.

The best travel insurance credit cards in Canada

Our Gold award for the #1 travel insurance card in Canada goes to RBC Avion Visa Infinite Privilege, thanks to its impressive 12 types of insurance and high-value coverage. Cardholders also benefit from powerful rewards with Avion points worth up to $2.33 when redeemed through the Avion Air Travel Redemption Schedule. To top it off, this card's welcome bonus is worth up to $1,631.

Our Silver award goes to the Scotiabank Passport Visa Infinite Privilege Card. This card also has 12 types of coverage. Plus, it includes airport lounge access and lucrative Scene+ points on groceries, dining, and entertainment purchases.

And our Bronze award goes to the CIBC Aeroplan Visa Infinite Privilege Card, which also offers 12 types of insurance, a welcome bonus valued at $1,600, and Aeroplan perks.

It's worth noting that all of Canada's top insurance credit cards are Visa Infinite Privilege cards, which come with premium annual fees.

In case you're looking for a more budget-friendly travel insurance card, we've also selected the top 3 insurance cards that charge lower annual fees.

Canada's best travel insurance credit card: RBC Avion Visa Infinite Privilege

×5 Award winner

×5 Award winner

The #1 credit card in Canada for insurance coverage – especially travel insurance – is the RBC Avion Visa Infinite Privilege. While all 3 of the top cards offer very similar insurance packages, this card offers slightly more for a lower annual fee of $399.

Most valuable coverage: 31 days of unlimited emergency medical insurance

Other top insurance cards offer 31 days, up to $5,000,000, which is the typical amount for this type of insurance.

The median number of days covered across Canadian credit cards is only 15, and some cards offer as few as 3, making the RBC Avion Visa Infinite Privilege a strong choice for travellers planning longer trips.

Given its high annual fee and income requirements, the fact that the RBC Avion Visa Infinite Privilege only earns 1.25 points per $1 spent on all purchases might seem low. But remember: RBC Rewards points are worth up to 2.33 cents each.

In fact, the RBC Avion Visa Infinite Privilege has the highest average rate of return of all the top insurance cards:

In addition to rewards, you'll enjoy Visa Infinite Privilege perks, including complimentary hotel upgrades, concierge services, and access to exclusive events.

With all these benefits, the RBC VIP more than earns its reputation as a top-tier premium credit card.

Insurance overview:

RBC Avion Visa Infinite Privilege

| Extended Warranty | 2 years |

| Purchase Protection | 120 days |

| Mobile Device | $1,500 |

| Travel Accident | $500,000 |

| Emergency Medical Term | 31 days |

| Emergency Medical Maximum Coverage | unlimited |

| Emergency Medical over 65 | 7 days |

| Trip Cancellation | $2,500 |

| Trip Interruption | $5,000 |

| Flight Delay | $1,000 |

| Baggage Delay | $750 |

| Lost or Stolen Baggage | $2,500 |

| Hotel Burglary | $3,000 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

Best travel insurance card silver winner: Scotiabank Passport® Visa Infinite Privilege* Card

In addition to offering one of Canada's best insurance packages, the Scotiabank Passport® Visa Infinite Privilege* Card doesn't charge a foreign transaction fee, making it an excellent choice if you're planning to shop abroad.

Most valuable coverage: Emergency medical over 65 (10 days)

It's hard to find credit card travel insurance if you're over 65 – and even harder to find a 10-day term, so the Scotiabank Passport® Visa Infinite Privilege* Card is a useful card to consider. For comparison, the #1 card on our list offers 7 days for emergency medical travel insurance over 65.

This card comes with a high annual fee of $599, but this is balanced by several perks. Start your trip with 10 free complimentary airport lounge visits via Visa Airport Companion, then shop to your heart's content with no currency exchange rate fees and up to 3x points per $1 spent on purchases.

Insurance overview:

Scotiabank Passport® Visa Infinite Privilege* Card

| Extended Warranty | 2 years |

| Purchase Protection | 180 days |

| Mobile Device | $1,000 |

| Travel Accident | $500,000 |

| Emergency Medical Term | 31 days |

| Emergency Medical Maximum Coverage | $5,000,000 |

| Emergency Medical over 65 | 10 days |

| Trip Cancellation | $2,500 |

| Trip Interruption | $5,000 |

| Flight Delay | $1,000 |

| Baggage Delay | $1,000 |

| Lost or Stolen Baggage | $2,500 |

| Hotel Burglary | $2,500 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

Best travel insurance card bronze winner: CIBC Aeroplan Visa Infinite Privilege Card

If you spend a lot on travel, especially if you're loyal to Air Canada, the CIBC Aeroplan Visa Infinite Privilege Card is a valuable travel insurance card for you. While the overall average return rate is slightly lower than the top card, the CIBC Aeroplan Visa Infinite Privilege Card offers a stronger travel return rate.

You can earn 2.4% on travel – boosted to 3.2% when you travel with Air Canada.

Most valuable coverage: Extended warranty

While the CIBC Aeroplan Visa Infinite Privilege Card has strong travel insurance, its most valuable coverage is extended warranty, which is valued at $144. This card offers 2 years of coverage. It also offers rental car coverage, valued at $140.

In total, you get 12 types of insurance, including double the length of emergency medical coverage on most cards, as well as 180 days (approximately 6 months) of protection for eligible new purchases against damage or theft.

Insurance overview:

CIBC Aeroplan Visa Infinite Privilege Card

| Extended Warranty | 2 years |

| Purchase Protection | 180 days |

| Mobile Device | $1,500 |

| Travel Accident | $500,000 |

| Emergency Medical Term | 31 days |

| Emergency Medical Maximum Coverage | $5,000,000 |

| Emergency Medical over 65 | 10 days |

| Trip Cancellation | $2,500 |

| Trip Interruption | $5,000 |

| Flight Delay | $1,000 |

| Baggage Delay | $1,000 |

| Lost or Stolen Baggage | $1,000 |

| Hotel Burglary | $2,500 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

The best travel insurance cards with lower annual fees

| Credit card | Annual fee | Types of coverage | Est. coverage value |

|---|---|---|---|

| National Bank World Elite Mastercard | $150 | 10/17 | $528 |

| TD First Class Travel Visa Infinite Card | $139 | 12/17 | $528 |

| BMO Ascend World Elite Mastercard | $150 | 12/17 | $528 |

If you live in Ontario, it's also worth checking out the Meridian Visa Infinite Cash Back Card and Meridian Visa Infinite Travel Rewards Card. These credit union credit cards offer 11 types of insurance for only $99, including rare price protection insurance.

National Bank World Elite Mastercard

The National Bank World Elite Mastercard is a fantastic dining credit card, but it also has impressive insurance coverage considering its annual fee. The card includes 10 types of insurance protections, including $1,000 of mobile phone coverage, up to $5 million in emergency medical coverage, and more.

Insurance overview:

National Bank World Elite Mastercard

| Extended Warranty | 2 years |

| Purchase Protection | 180 days |

| Mobile Device | $1,000 |

| Emergency Medical Term | 60 days |

| Emergency Medical Maximum Coverage | $5,000,000 |

| Emergency Medical over 65 | 15 days |

| Trip Cancellation | $2,500 |

| Trip Interruption | $5,000 |

| Flight Delay | $500 |

| Baggage Delay | $500 |

| Lost or Stolen Baggage | $1,000 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

Even better, cardholders are reimbursed up to $150 annually for travel expenses, including airport parking, baggage fees, and seat selection or upgrades. Cardholders also enjoy unlimited access to the National Bank international airport lounge in Montreal and a Mastercard Travel Pass membership.

TD First Class Travel Visa Infinite Card

$40 GeniusCash + Up to 146,000 TD Rewards points (conditions apply).*

$40 GeniusCash + Up to 146,000 TD Rewards points (conditions apply).*

The TD First Class Travel Visa Infinite Card is a solid card for luxury travellers on a budget. Its annual fee of $139 is lower than top insurance cards, yet it still provides 10 types of protections.

Plus, there are two ways you can get all or most of your annual fee back. For the first year, you can get a rebate. And every year, you get a $100 travel credit (on a purchase of $500 or more) that offsets just over 2/3 of the fee.

Insurance overview:

TD First Class Travel® Visa Infinite* Card

| Extended Warranty | 1 year |

| Purchase Protection | 90 days |

| Mobile Device | $1,000 |

| Travel Accident | $500,000 |

| Emergency Medical Term | 21 days |

| Emergency Medical Maximum Coverage | $1,000,000 |

| Emergency Medical over 65 | 4 days |

| Trip Cancellation | $1,500 |

| Trip Interruption | $5,000 |

| Flight Delay | $500 |

| Baggage Delay | $1,000 |

| Lost or Stolen Baggage | $1,000 |

| Hotel Burglary | $2,500 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

The TD First Class Travel Visa Infinite Card also offers Visa Airport Companion membership with 4 free passes and a birthday bonus of up to 10,000 points.

BMO Ascend World Elite Mastercard

The BMO Ascend World Elite Mastercard has an impressive 12 types of insurance for its annual fee of $150. Plus, you get the first year free, so you can decide if the card is right for you.

Insurance overview:

BMO Ascend™ World Elite®* Mastercard®*

| Extended Warranty | 1 year |

| Purchase Protection | 90 days |

| Travel Accident | $500,000 |

| Emergency Medical Term | 21 days |

| Emergency Medical Maximum Coverage | $5,000,000 |

| Trip Cancellation | $1,500 |

| Trip Interruption | $2,000 |

| Flight Delay | $500 |

| Baggage Delay | $500 |

| Lost or Stolen Baggage | $500 |

| Personal Effects | $750 |

| Hotel Burglary | $1,000 |

| Rental Car Theft & Damage | Yes |

Please review your insurance certificate for details, exclusions and limitations of your coverage.

This card earns BMO Rewards, which are flexible but have a relatively low point value, maxing out at 0.67 cents per point.

Cardholders can also enjoy World Elite Mastercard perks, including 4 lounge passes through Mastercard Travel Pass.

Compare all travel insurance credit cards by Genius Rating

Our Genius Rating system uses a refined, math-based algorithm that analyzes over 126 data points to generate a score out of 5 for every credit card we review.

The Genius Rating methodology

The Genius Rating methodology evaluates cards by the following criteria:

- Insurance

- Rewards

- Fees

- Perks

- Interest rates

- Acceptance

- Approval

To rank the top insurance cards in Canada, we prioritize each card's insurance score. To score well on insurance, a card needs both a wide range of coverages and competitive amounts in each area.

Learn more about our Genius Rating methodology

How to choose the right travel insurance credit card

Choosing the right travel insurance credit card starts with a quick self‑assessment. Review how you typically travel – whether solo or in a group, preferred destinations, modes of transport, and trip length. Then match those habits to your insurance needs, considering your financial situation and the level of coverage you'd want in a worst‑case scenario.

Make sure your card's policy actually covers your specific situation: Read the fine print for age limits, trip duration, destination exclusions and any annual or lifetime caps.

Finally, weigh the rewards and other benefits. If two cards meet your coverage criteria, pick the one that aligns best with your everyday spending and offers redemption options you'll actually use.

Remember: Check exactly what you need to charge to your card in order to be eligible for travel insurance. You aren't automatically eligible just by being a cardholder. You often need to charge all – or at least most – of your trip to your card in order to insure it.

Insurance

There are a total of 17 types of credit card insurance available in Canada, each with its own benefits, exemptions, and limitations.

The top-ranked insurance cards in the country have comparable insurance packages, each offering similar coverage. But each card has its own standout areas.

Here's how our top travel insurance cards compare, alongside one of the best lower-fee travel insurance cards:

| RBC Avion Visa Infinite Privilege | Scotiabank Passport Visa Infinite Privilege Card | CIBC Aeroplan Visa Infinite Privilege Card | National Bank World Elite Mastercard | |

|---|---|---|---|---|

| Extended warranty | 2 years | 2 years | 2 years | 2 years |

| Purchase protection | 120 days | 180 days | 180 days | 120 days |

| Travel accident | $500,000 | $500,000 | $500,000 | N/A |

| Emergency medical coverage | Unlimited | $5,000,000 | $5,000,000 | $5,000,000 |

| Emergency medical term | 31 days | 31 days | 31 days | 60 days |

| Trip cancellation/interruption | $2,500; $5,000 | $2,500; $5,000 | $2,500; $5,000 | $2,500; $5,000 |

| Flight delay | $1,000 | $1,000 | $1,000 | $500 |

| Baggage delay | $750 | $1,000 | $1,000 | $500 |

| Lost or stolen baggage | $2,500 | $2,500 | $1,000 | $1,000 |

| Hotel burglary | $3,000 | $2,500 | $2,500 | N/A |

| Rental car | Yes | Yes | Yes | Yes |

| Mobile device | $1,500 | $1,000 | $1,500 | $1,000 |

While the National Bank World Elite Mastercard doesn't offer as comprehensive insurance as some of the other picks, it is the only card to provide 60 days of emergency medical care – almost double its rivals. However, this card is missing travel accident insurance.

Rewards

Since the best-ranked insurance credit cards have very competitive coverage, it's worth taking a look at which one will get you the best rewards.

Consider the overall average return rate as well as the return rate for travel purchases.

| Credit card | Average return rate | Travel return rate | Annual fee |

|---|---|---|---|

| RBC Avion Visa Infinite Privilege | 2.91% | 2.91% | $399 |

| Scotiabank Passport Visa Infinite Privilege Card | 1.18% | 3% | $599 |

| CIBC Aeroplan Visa Infinite Privilege Card | 2.22% | * 2.4% * 3.2% when booking with Air Canada | $599 |

Tip: No matter what credit card you use, you could be earning bonus cash back on top of your card's rewards. Input your monthly spend in the GeniusCash app, and level up to earn real cash.

Fees

As Visa Infinite Privilege cards, all of the top three insurance cards have premium annual fees:

- RBC Avion Visa Infinite Privilege – $399

- Scotiabank Passport Visa Infinite Privilege Card – $599

- CIBC Aeroplan Visa Infinite Privilege Card – $599

However, you can find cards with standard annual fees that offer solid insurance packages:

- National Bank World Elite Mastercard – $150

- TD First Class Travel Visa Infinite Card – $139 (first year rebate available)

- BMO Ascend World Elite Mastercard – $150 (waived for the first year)

When choosing a card you plan to travel with, it's also important to consider foreign transaction fees. Most Canadian cards add a 2.5% surcharge on every purchase made in a non‑CAD currency.

The Silver-award-winning Scotiabank Passport Visa Infinite Privilege Card is the only card in this guide that doesn't charge a foreign transaction fee.

Looking for a card to shop abroad? Check out the best credit cards with no FX fees.

Perks

Credit cards with exceptional travel insurance often offer travel perks and benefits for cardholders.

Perhaps the most luxurious of the travel-centric perks is airport lounge access, either through Priority Pass, DragonPass, or via an airline (like Air Canada's Maple Leaf Lounges). Lounge access is usually around $35 per visit (plus guests), so these complimentary passes can be extremely valuable to the regular traveller.

- The RBC Avion Visa Infinite Privilege offers 6 lounge passes through DragonPass, plus fast track security and priority airport parking at select Canadian airports.

- The Scotiabank Passport Visa Infinite Privilege Card provides 10 free passes to Visa Airport Companion lounges and a $250 travel credit.

- The CIBC Aeroplan Visa Infinite Privilege Card gives you unlimited Maple Leaf lounge access and free checked bags on Air Canada.

The National Bank World Elite Mastercard also offers lounge access, though greatly reduced. Cardholders enjoy access to the National Bank Lounge at Montréal-Trudeau Airport, which is wonderful, but unless you live in (or travel to/from) Montreal, it offers limited value. Instead, National Bank makes travel more affordable with a $150 annual travel credit towards incidentals like airport parking, baggage, or seat selections.

The best travel insurance cards also provide perks outside of what you'd typically expect from a "travel credit card."

The RBC Avion Visa Infinite Privilege, for example, offers partner benefits, including international data thanks to two 1 GB/15-day complimentary GigSky eSim data plan passes, Visa Infinite features such as golf perks at 150 global courses, Visa concierge, and access to the Visa Hotel Collection, a free 12-month DashPass membership with DoorDash, 20% savings at Hertz Rent-A-Car locations, and savings of 3¢/L on fuel at Petro-Canada locations.

Interest rates

All the best insurance credit cards have fairly standard purchase interest rates:

- RBC Avion Visa Infinite Privilege – 20.99%

- Scotiabank Passport Visa Infinite Privilege Card – 20.99%

- CIBC Aeroplan Visa Infinite Privilege Card – 21.99%

- National Bank World Elite Mastercard – 20.99%

- TD First Class Travel Visa Infinite Card – 21.99%

- BMO Ascend World Elite Mastercard – 21.99%

Acceptance

Another good thing about the best travel insurance cards is that you shouldn't have to worry about acceptance, no matter which card you pick. Both Visa and Mastercard are widely accepted.

Approval

Of course, you'll need to make sure you qualify for your ideal card.

| Credit card | Income requirements | Estimated credit score |

|---|---|---|

| RBC Avion Visa Infinite Privilege | $200,000 personal or $200,000 household | 660 – 724 |

| Scotiabank Passport Visa Infinite Privilege Card | $150,000 personal or $200,000 household | 760 – 900 |

| CIBC Aeroplan Visa Infinite Privilege Card | $150,000 personal or $200,000 household | 760 – 900 |

| National Bank World Elite Mastercard | $80,000 personal or $150,000 household | 760 – 900 |

| TD First Class Travel Visa Infinite Card | $60,000 personal or $100,000 household | 660 – 724 |

| BMO Ascend World Elite Mastercard | $80,000 personal or $150,000 household | 560 – 659 |

How travel credit card insurance works

There are 17 types of credit card insurance available in Canada.

| Insurance coverage | Estimated value | What it covers |

|---|---|---|

| Theft and damage to rental car insurance | $140 | Charges relating to the damage or theft of a rental car |

| Emergency medical coverage | $119 | Emergency medical attention and related expenses |

| Extended warranty | $78 | Repairs or the replacement of a defective item after the original manufacturer's warranty has expired |

| Price protection | $72 | The difference between the current price of an item and what you paid for it before it went on sale |

| Mobile device | $53 | Accidentally damaged, lost, or stolen mobile devices (minus a deductible and depreciation) |

| Trip cancellation | $39 | The costs of your travel tickets if bereavement, illness, or other reasons force you to cancel your trip |

| Purchase protection | $38 | Damaged, lost, or stolen recent purchases |

| Trip interruption | $26 | The costs of returning home if an accident, death, or illness forces you to end your trip early |

| Personal effects | $23 | Personal belongings damaged, lost, or stolen while on vacation |

| Rental car accident | $19 | A lump sum payment if the passengers in a rental car suffer death or injury |

| Travel accident | $9 | A lump sum payment if you or your family suffer death or dismemberment while on vacation |

| Baggage delay | $8 | Clothes and other necessities if your luggage is delayed by the airline |

| Event tickets | $8 | The cost of your tickets if the event is cancelled or you can't go |

| Flight delay | $6 | Food, lodging, and other necessities if your flight is delayed (may be combined with airline delay compensation) |

| Hotel burglary | $2 | Personal items stolen from your hotel room |

| Lost or stolen baggage | $2 | Lost or stolen airline luggage |

| Rental car personal effects | $2 | Personal items damaged in or stolen from a rental car |

A travel insurance credit card provides the cardholder (and sometimes their spouse, dependent children, and/or car passengers) with insurance coverage during travel outside the province or country.

To submit a claim, you must follow the instructions and terms and conditions outlined in your credit card's insurance agreement. Not every injury, loss, theft, or purchase is covered, and even successful claims are usually limited to a specific dollar amount.

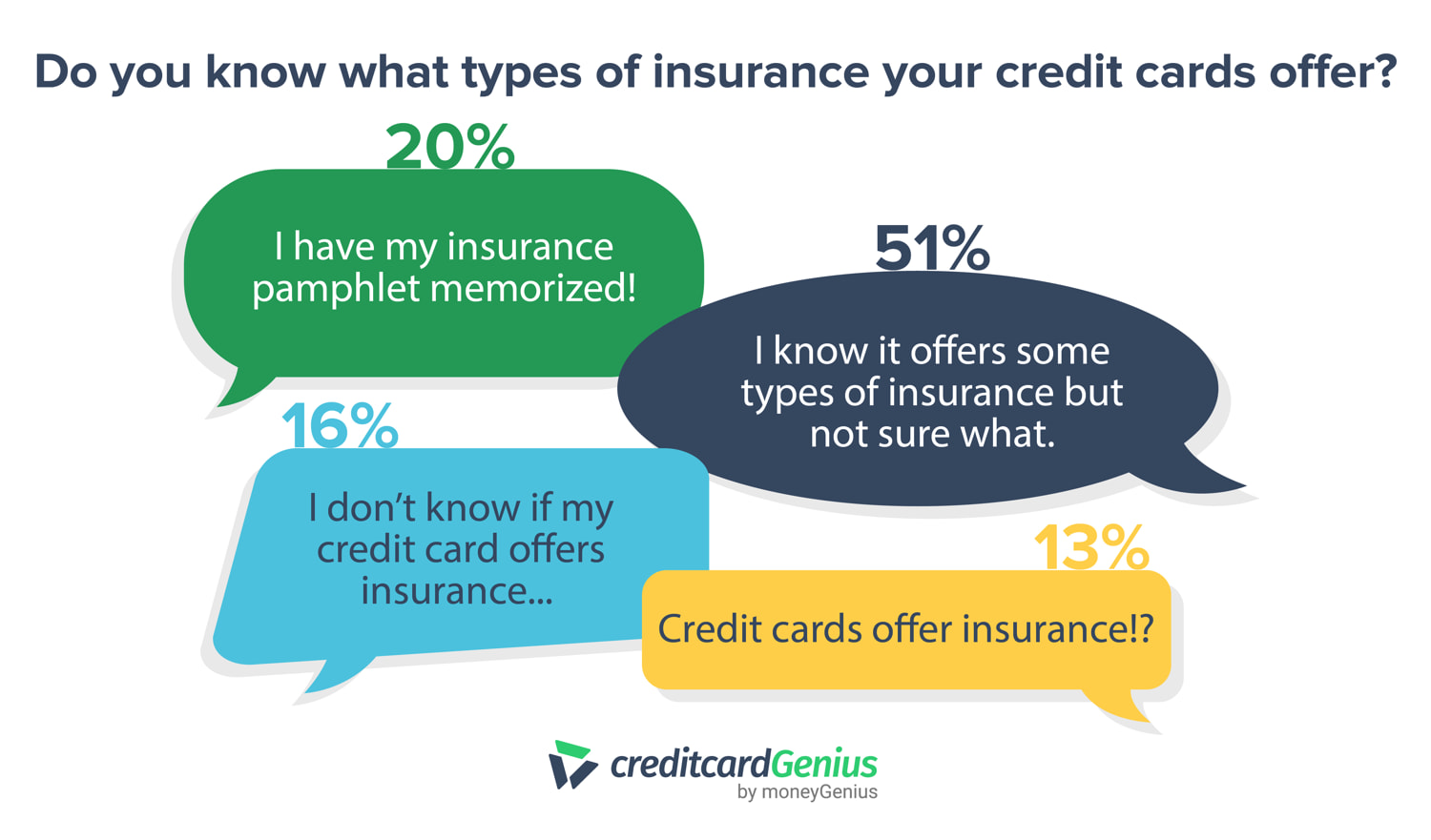

Do you know what types of insurance your credit cards offer? We surveyed Canadians and found that while 20% know their insurance package inside out, 29% aren't familiar with their coverage.

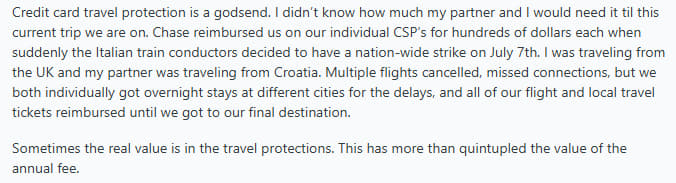

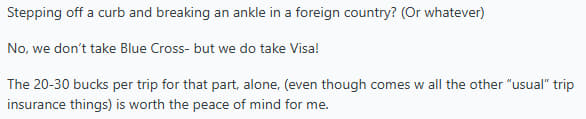

Real-life cases of credit card travel insurance

We turned to Reddit for examples of people using their credit card insurance while travelling.

This traveller's trip was impacted by a train conductor strike, which caused them to miss or cancel several parts of their vacation:

Another user mentioned using their travel coverage for an issue with their rental car:

And this Redditor used their card's medical coverage while abroad:

While all these examples prove that travel insurance comes in handy, another Redditor pointed out that it's up to you to learn about your coverage.

Common travel insurance exclusions

Travel insurance covers a lot, but it won't cover everything. Here are some situations where your insurance coverage may not be valid:

- Pre-existing medical conditions: Most credit card insurance won't cover medical expenses related to pre-existing conditions before your trip – sometimes up to six months prior. If you have an ongoing health concern, review your insurance policy carefully and consider purchasing additional coverage.

- High-risk activities: While exciting, activities like skydiving and scuba diving may not be covered by credit card insurance. You may need separate coverage that is tailored to these risks.

- Insufficient documentation: All claims require documentation to be submitted within a specified time period for processing. Keep all receipts, medical records, and other relevant documents and submit them as instructed by your issuer/provider. Failure to do so may result in the denial of your claim.

- Failure to charge travel to the card: For credit card insurance to apply, you must charge the full cost of your trip to it. If you pay for your trip with multiple payment methods, you may not receive full coverage.

- Age restrictions: In emergency medical cases, age limits may apply to coverage. Confirm the details on your insurance certificate and purchase additional coverage before travel, if required.

- Acts of war or terrorism: Most credit card insurance policies exclude coverage for events related to war or terrorism. If you're travelling to an area where this could be a risk, consider purchasing separate coverage.

FAQ

What are the most common travel insurance claims?

The most common travel insurance claims are for flight delays. However, claims for lost or delayed baggage, medical expenses, and trip cancellations are still very common. It's not unusual for a traveller to have to file multiple claims.

Are you automatically covered by your credit card insurance?

Yes, your credit card insurance will automatically apply to purchases you make with the credit card. For example, if you purchase a flight and pay with your card, the travel insurance offered by the card is valid for that purchase.

Where can you use your travel insurance coverage?

The most common place you'll use your travel insurance coverage is the airport, where insurance can cover trip cancellations or interruptions. Once you've arrived at your destination, you can use your travel insurance at rental car agencies, hotels, and even foreign hospitals – assuming your credit card includes these coverages.

Is there a time limit to file a travel insurance claim?

Your card's terms and conditions will provide the specific details, but generally, travel insurance time limits range from one week to 30 days. In any case, you can always call for immediate emergency assistance using your Canadian health card.

Are there age limits on travel insurance?

Most credit cards extend travel insurance to Canadians below the age of 65. Only a few cover travellers up to the age of 74, and even fewer extend to seniors over the age of 75.

Do I have travel insurance with my Visa credit card?

Few free and low-fee Visa Classic and Gold credit cards include travel insurance, but many Visa Platinum, Infinite, and Infinite Privilege cards do. To verify your travel coverage, contact your credit card issuer or review your card's insurance agreement.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.