Occasionally, you might spot errors on your credit card statement – like being billed twice or being charged for a service you didn’t actually receive. Whatever the reason, if you see a charge that you didn’t initiate and the merchant can’t rectify it, you can reach out to your card provider and request a chargeback – a credit reversal.

As long as you meet the issuer’s qualifications, you won’t be required to pay for the item or service. We’ll walk you through the process so you can dispute the charge and have it reversed.

Key Takeaways

- A credit card chargeback is a reverse transaction on something you purchased.

- You should only initiate a chargeback after you speak to the merchant to resolve the situation.

- Banks will only approve chargebacks for specific reasons – and usually only after they complete an investigation into the issue.

Never miss an amazing deal again + get our bonus 250+ page eBook for FREE. Join 50,000 other Canadians who receive our weekly newsletter – learn more.

What is a credit card chargeback?

A credit card chargeback is a reverse transaction on something you purchased. So, a chargeback credits your account if a seller hasn’t fulfilled a service or provided a product.

Although credit card chargebacks are rare, they can be an effective form of purchase protection if you can’t resolve the problem with the merchant directly.

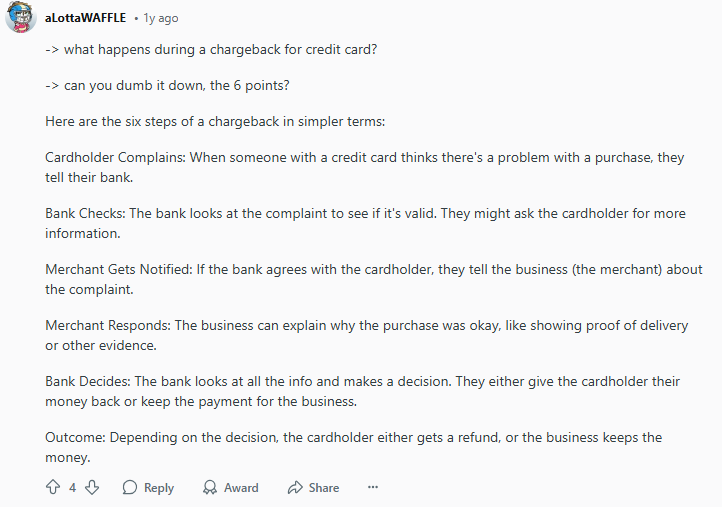

As this Redditor explained, it’s a simple process of around 6 steps:

Bank chargeback policies in Canada

If you have a dispute on your credit card or are the victim of credit card fraud, you probably want to resolve it as quickly as possible. To make the process easier, we’ve put together a useful reference table so you can quickly contact your bank and get a reversal as soon as possible.

| Bank | Policy | Phone number | More info |

|---|---|---|---|

| BMO | * Cardholders have the right to dispute any credit card transactions within 30 days of the statement date * You can start the process through your BMO online banking | 1-877-225-5266 | More info |

| CIBC | * Cardholders have the right to dispute any credit card transactions within 30 days of the statement date * Call CIBC Credit Card Services or sign in to your CIBC online banking to start the process | 1-800-465-4653 | More info |

| Scotiabank | * If you were charged for merchandise you didn't receive or for services not received on or after the service date, you can dispute the charge * Call Scotiabank customer service to start the process | 1-800-504-0716 | More info |

| RBC | * If you didn't receive a product or service you paid for, were charged for cancelling a service, or were charged twice, you can dispute the charge * You can start the process through your RBC online banking or mobile app | 1-800-769-2512 | More info |

| TD | * If you are unable to resolve the dispute with the merchant, submit a transaction dispute request with TD within 30 days of your statement date * Call TD customer support directly, or start a dispute claim through your TD online banking | 1-800-983-8472 | More info |

If your bank or credit card issuer isn't listed here, chances are good that you'll be able to find dispute resolution information on their website or through your online banking portal.

Why you might need to do a credit card chargeback

Just because you can request a credit card chargeback doesn’t mean your bank will automatically reverse the charges.

Usually, banks will only approve a chargeback for one of the following reasons:

- There's an unauthorized transaction on your card

- You've been double-charged for the same transaction

- You were charged the wrong amount

- You don't recognize the charge

- You're still being charged for a service you cancelled

- You did not receive a product or service you paid for

Some issuers may have additional reasons but for the most part, these are the sorts of things for which you can request credit card chargebacks.

Some of the instances where your credit card issuer won’t do a chargeback include:

- You miss your flight (or boat, bus, train, etc.)

- You are charged for a hotel booking that you forgot to cancel

- You get sick (or miss your flight) and can't attend a concert

- A product is broken (regardless of whose fault – this is where warranties come in handy)

If you're in doubt, you can request a chargeback – but be sure to check the fine print, however, since some issuers will charge a fee if your chargeback request is invalid.

How to initiate a credit card chargeback

To help you get started, we’ve simplified the process for requesting a credit card chargeback.

1. Check your credit card statement carefully

It’s always a good idea to check your credit card statement throughout the month since it’s easier to catch fraudulent transactions or phishing scams.

If you use online banking, log in and take a few moments to check your transactions. Look for unusual transactions that you didn’t authorize. If you see a transaction with a company you’ve never heard of, you’ll want to look deeper into it.

You’ll also want to pay attention to purchases you’ve made but haven’t received yet.

2. Research strange transactions

If there's a charge on your credit card that you're not sure about, run through this list to see if you can figure it out on your own.

- If you don't recognize the amount of the charge, were there any additional fees involved (e.g., currency exchange fees, foreign transaction fees, etc.)?

- If you didn't purchase anything on that date, did you make an earlier purchase that just wasn't put through for a day or two?

- If you didn't purchase anything at a particular location, did you make a purchase at another location of the same shop?

- If you don't recognize a merchant name, keep in mind that sometimes merchants change their name or have a different name for their credit card account.

- If you don't recognize a purchase at all, do you have any authorized users on your account? Did they make the purchase?

- If not, is it a recurring charge you forgot about? Or maybe a free trial you signed up for but forgot to cancel before being charged?

If you still haven't figured it out, it's time to make some calls.

3. Contact the merchant

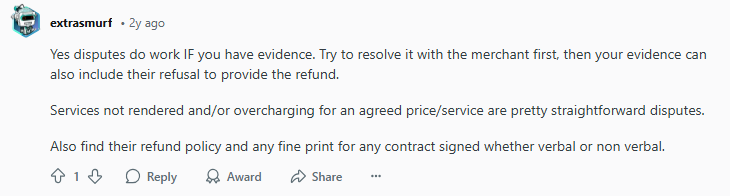

Most banks expect you to contact the merchant before filing a dispute, and most sellers want to find a solution that makes you happy. They don’t want negative publicity or the loss of your business – especially if there was a simple mistake with your order.

In some cases, the merchant might send you a replacement item, offer a refund, or give you the option to have credit. If they don’t come up with a solution that you’re happy with, you might proceed with a credit card dispute to get your money back.

Pro Tip: Always take clear, detailed notes. Write down the date and time of all communications, which customer service rep you were speaking with, notes from the discussion, and any takeaways or action items. These notes might come in handy if you file a dispute with your credit card company.

4. Collect evidence

Your credit card company might ask for evidence like receipts, invoices, or notes of conversations you’ve had with the merchant. They might ask you to forward emails or send screenshots of communications to help them investigate your dispute.

6. Request a chargeback from your credit card issuer

If you get your credit card statement and you notice something's off, you should look into acting fast. Most credit card companies only allow you to initiate a chargeback within a certain amount of time – typically 30 days from the date you get your credit card statement.

Once you’ve contacted the merchant and gathered evidence, call your credit card issuer's customer support line or submit a request online. Some issuers will let you submit chargeback requests on their mobile app, too.

7. If that fails, contact an ombudsman

If your credit card issuer rejects your request for a chargeback but you still believe you're entitled to one, you can ask an external ombudsman for help. One such organization is the ADR Chambers Banking Ombuds Office (ADRBO), which reviews complaints against member banks.

3 things NOT to do during a chargeback

Here are a few tips about what to avoid doing in these situations.

Don't request a chargeback before talking to the retailer

One of the first questions that you'll be asked is whether you tried talking to the vendor, so do this before you contact your bank.

If you haven’t spoken with the merchant’s customer service, your credit card company probably won’t go ahead with your request.

Don't refuse to pay your credit card bill

Until credit card disputes are resolved, you are still 100% responsible for any charges that appear on your credit card statement. If you refuse to pay them, you’ll have to pay interest and your credit score may take a hit.

Pay your credit card bills on time and in full, even if you're disputing a transaction.

If you get your money back, you will see an adjustment on your credit card statement that is equal to the amount that you disputed. You may even get a "temporary" adjustment if the dispute is being drawn out – but keep an eye on your statements in case your credit card chargeback is denied.

Don't lie or make false claims

Don't lie about anything when going through a credit card chargeback process. At some point you may be asked to sign a sworn statement that everything you're saying is true – if it's not, there could be serious legal consequences.

Does a chargeback always work?

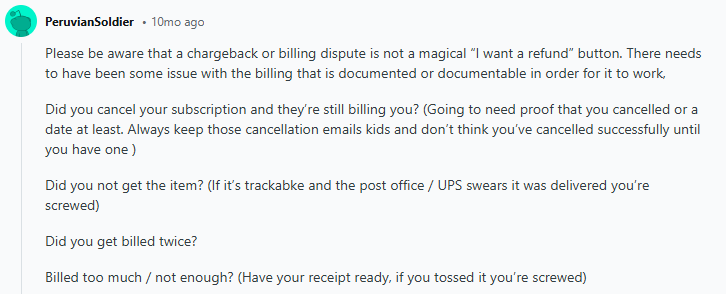

According to Shopify, cardholders have an 88% success rate in successfully resolving a chargeback. That said, merchants might refuse your chargeback request if they believe it doesn’t qualify.

If your chargeback is denied, you’ll be expected to pay for the transaction plus any interest that’s accrued in the meantime. If the merchant suspects fraud, they have the right to begin legal proceedings.

FAQ

What happens if you do a credit card chargeback?

You’ll submit a request with your credit card company and they’ll investigate your dispute. While it might take a few weeks, they’ll either reverse the charge or let you know why your request was denied.

How do you qualify for a credit card chargeback?

You’re allowed to request a credit card chargeback as long as it’s for a qualifying reason. For instance, if you didn’t authorize a payment or purchase, or you see you were charged twice for the same item, you may qualify for a chargeback.

How do I initiate a PayPal or Shopify chargeback?

If you paid for something using PayPal, you can also initiate a chargeback. The process is the same as if you were to dispute a credit card charge normally. Your credit card issuer will communicate with PayPal and work with them to get your money back.

How successful are credit card chargebacks?

Success depends on why you’re requesting a chargeback. If the merchant was clearly at fault and you haven’t been able to resolve the matter with them, most credit card companies will reverse the charge. Banks will take time to thoroughly investigate the charge and they won’t approve a chargeback request that doesn’t qualify.

Does doing a credit card chargeback hurt your credit score?

A credit card chargeback will not hurt your credit. But if you refuse to pay for the charge on your credit card statement while waiting for a dispute to be resolved, your credit score could take a hit – even if the transaction is later reversed.

creditcardGenius is the only tool that compares 126+ features of 251 Canadian credit cards using math-based ratings and rankings that respond to your needs, instantly. Take our quiz and see which of Canada's 251 cards is for you.

GC:

GC:

Comments

Leave a comment

Required fields are marked with *. Your email address will not be published.

Showing 8 comments