In a KOHO vs. Neo showdown, KOHO comes out on top, mostly thanks to its ease of use and variety of products. Both require memberships to help build your credit score, and KOHO's fees are lower.

This article compares Neo and KOHO, specifically across categories such as cash back, monthly fees, and interest rates. We'll also explain the additional services each offers, so you can work with a company that has everything you're looking for.

Key Takeaways

- KOHO offers 3 tiers of service plans, ranging from free to $14.75 per month.

- Neo has 3 membership plans, but only 2 give you the opportunity to improve your credit score.

- To choose the best option, determine what products and services you need and what you're willing to pay.

Never miss an amazing deal again + get our bonus 250+ page eBook for FREE. Join 50,000 other Canadians who receive our weekly newsletter – learn more.

What we love about KOHO

KOHO is a Canadian fintech company that only operates online – no physical stores are available in Canada. It offers a hybrid chequing/savings account that comes with a prepaid credit card you can use to make purchases, and using this account responsibly can help you build your credit score.

KOHO also offers:

- Prepaid travel card: KOHO's newest prepaid offering is a travel Mastercard that includes a free eSIM for travelling abroad. You'll also avoid foreign exchange (FX) fees, get fraud protection, and enjoy travel offers from partners like Expedia and Booking.com.

- Credit building: This service helps you build your credit score while meeting personal financial goals. It's essentially a tiny personal line of credit that allows you to build positive payment history and increase your credit score.

- Cash advances: Subscribe to the Cover bundle and get access to an instant, interest-free cash advance of up to $250. The plan also includes a free credit report and access to financial coaching.

- Lines of credit: Apply for a line of credit through KOHO's partner, Fora. If approved, you can get a line of credit of $1,000 – $15,000. As a line of credit, you'll only pay interest on the actual amount of credit you use.

- Buy now pay later: Break a large purchase into smaller, equal monthly payments for a small fee. By repaying the purchase with a 3, 6, or 9-month term, you could save on the interest you would have been charged.

- International money transfers: Get the best rate when sending money abroad, since KOHO uses the live exchange rate. KOHO's transfer fees are low, and funds move within minutes.

- Crypto: With low trading fees, you can make crypto purchases directly from your KOHO account. You won't pay any FX fees because all coins are paired with CAD.

| Pros | Cons |

|---|---|

| Services tailored for newcomers and those building credit | Monthly fee required to access all credit building and account features |

| Earn high interest rates on account balances | Fees for ATM use |

| Access to financial advisors and credit building tools/education | No personalized product recommendations |

| Highly-rated app with budgeting and goal setting features |

What we love about Neo Financial

In the other corner is Neo Financial, another Canadian fintech that offers personal finance products. While it used to offer hybrid accounts, clients can now select a separate chequing or savings account from Neo.

Its lineup of services is pretty extensive:

- Mortgages: Get pre-qualified online in minutes for mortgages with terms up to 5 years. Then, work with an agent online or over the phone to submit documents and get your loan.

- Credit cards: Whether you're looking for a cash back credit card, a credit card with travel benefits and perks, or a card that helps you build your credit score, Neo has you covered.

- Investments: With personalized portfolios through OneVest, account managers work behind the scenes to help clients achieve their investment goals.

| Pros | Cons |

|---|---|

| Includes a virtual credit card you can begin using before your physical card arrives | Requires a high minimum balance to earn the best interest rate |

| No monthly chequing account fees | Chequing and savings accounts are separate |

| Offers mortgages for new homeowners or those looking to renew their loans | No ability to deposit cash or cheques |

| Can combine savings balances with another account holder |

KOHO vs. Neo: Interest rates

KOHO has a dedicated high interest savings account (HISA) that's free to open and requires no minimum balance. When you open the account, you'll select a goal/plan that determines your exact interest rate. These HISAs have interest rates that range from 0.5% to 3.5% – sometimes even higher with promotional offers.

Be aware that the balance in your KOHO chequing accounts also earns interest, which depends on your KOHO plan. For instance, you'll earn 2% interest with a free KOHO Essential Plan, but Everything Plans earn 3.5% on your balance.

Neo also pays interest on your chequing account balance, but just 0.1%. Its HISA earns more, but this Neo account is tiered, with rates ranging from 2% to 2.75%. You'll need at least $20,000 in your account to get the best interest rate.

| KOHO | Neo | |

|---|---|---|

| HISA interest rate | 0.5% – 3.5% | 2.25% – 2.75% |

| Interest earned on chequing account balance | 2% – 3.5% | 0.1% |

Winner: KOHO

KOHO vs. Neo: Cash back

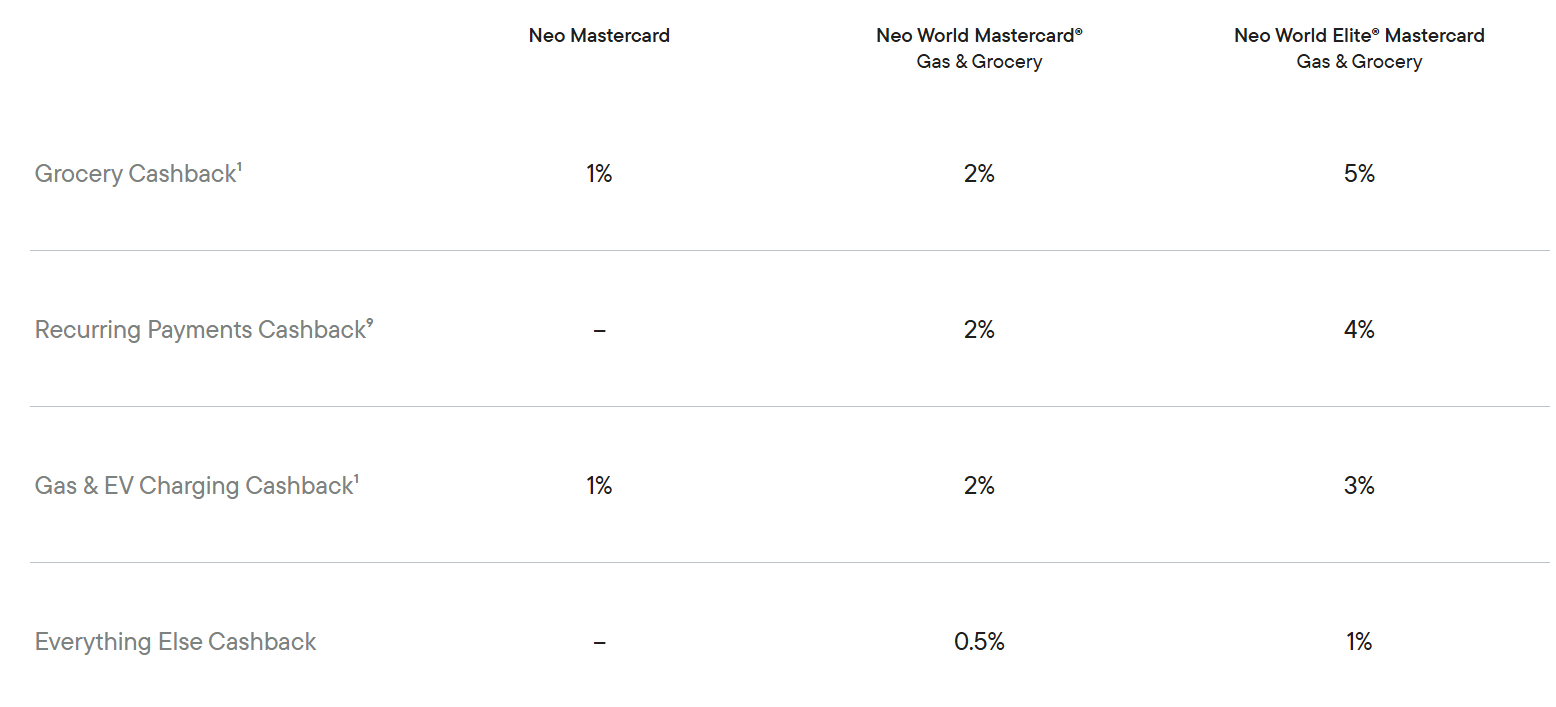

It's tough to choose the better option in the cash back category. Neo recently changed its reward structure for cash back, but you'll earn anywhere from 0.5% to 5% cash back, plus up to 15% back when you shop with Neo partners:

With KOHO, the cash back you earn depends on your plan – Essential, Extra, or Everything. Instead of earning cash back based on purchase category or partner, you'll earn 1% to 2% on everything you buy.

The winner: Tie

KOHO vs. Neo: Credit cards

KOHO doesn't offer many credit cards. You're basically issued a prepaid Mastercard that matches the KOHO plan you sign up for:

On the other hand, Neo has a solid lineup of Mastercards, both secured and unsecured, that include Mastercard benefits, cash back, and travel offers.

Here are some of your Neo credit card options, which don't include secured cards:

Neo also works with United Airlines and Cathay Pacific to offer co-branded cards.

With its extensive lineup and credit cards tailored to just about anyone's needs, Neo wins this category.

The winner: Neo

KOHO vs. Neo: Credit building

Both KOHO and Neo use similar credit-building strategies. With KOHO, you choose a membership plan/tier, which may or may not include a discount for the KOHO Credit Building service. With this service, your monthly payment is reported to Equifax, which can help you improve your score.

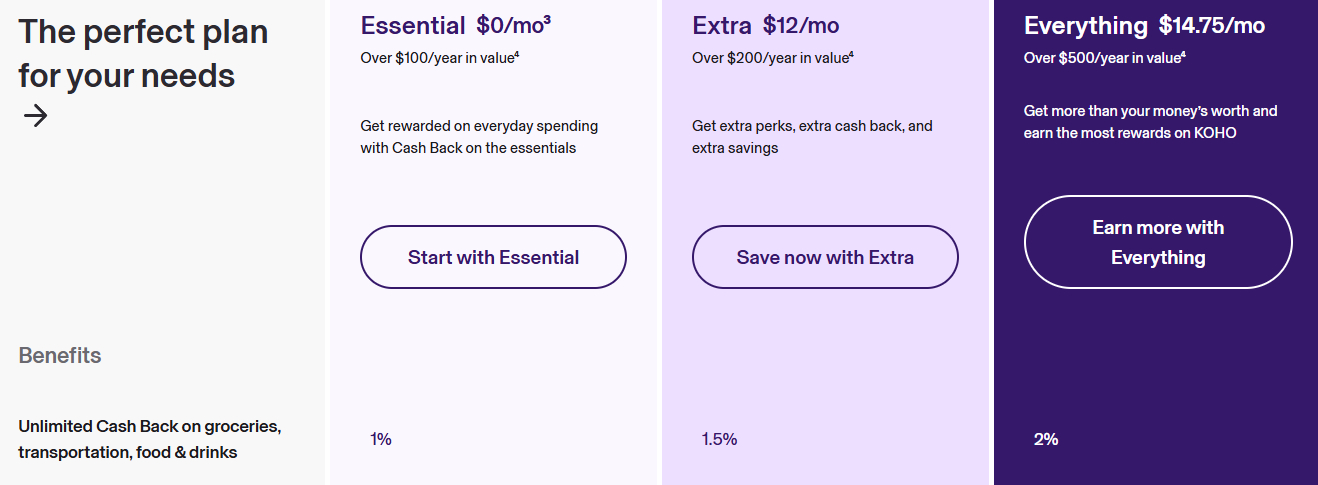

Each KOHO membership level offers different features, with the premium level giving you the most perks:

- Essential: Free credit score, instant e-transfers, 1% cash back on groceries, transportation, food and drink, 2% interest on your prepaid balance

- Extra: Same as Essential, plus better cash back and interest rates, no foreign exchange fees, 30% discount on credit building

- Everything: Same as Extra, plus the best interest rates and cash back rates, 50% discount on credit building

Neo also offers plans, but only 2 of them can help you build your credit by reporting payments to TransUnion:

- Build: 2.5% interest on savings, credit score monitoring, ATM fee reimbursement, free transactions, financial insights

- Grow: Same as Build, but 2.75% interest on savings, plus no foreign exchange fees, premium support

The winner: KOHO

KOHO vs. Neo: Monthly fees

Now that you know a little about how these companies structure their credit building tools, see how much they charge for them.

KOHO:

- Essential: $0 if you set up direct deposit in any amount or add at least $1,000 to the account

- Extra: $12 per month

- Everything: $14.75 per month

Neo:

- Build: $0 to $7.99 per month

- Grow: $0 to $12.99 per month

Enjoy a free membership if you have $5,000 in your Build account or $20,000 in your Grow account. You'll also get a free Build membership if you have an unsecured World Elite Mastercard issued by Neo.

The winner: KOHO

KOHO vs. Neo: Mobile apps

It's close, but KOHO takes a slight lead when it comes to mobile app scores. Reviewers note that the app has become easier to use over the years and that more features have been added, making it easier to do their banking on the go.

Neo's scores lag behind when it comes to the Google Play app. Users say their data has been compromised and that cash-back opportunities have been misleading.

| KOHO | Neo | |

|---|---|---|

| App Store | 4.8 | 4.8 |

| Google Play | 4.7 | 4.3 |

The winner: KOHO

Overall winner: KOHO

KOHO wins this competition, but we have to admit that it's tricky to compare credit-building tools like these. Both Neo and KOHO offer different services, and their plans are structured differently, with unique opportunities to waive their plan fees.

That said, KOHO makes it easier and more affordable for most Canadians to take the initial steps of building their credit. If you're primarily interested in building your credit with a credit card, though, don't overlook Neo's impressive card lineup.

Best alternative: Wealthsimple

You might initially think of Wealthsimple as an investment company, but it holds its own against KOHO and Neo. Wealthsimple offers:

- Retirement accounts

- Mortgages

- Business accounts

- Tax advice

- Chequing accounts

- Credit-building tools

| Wealthsimple chequing | |

|---|---|

| Monthly fee | $0 |

| Foreign exchange fees | $0 |

| Interest rate | Up to 2.25% |

| ATM fees | Reimbursed by Wealthsimple |

| E-transfer limits | Up to $50,000 a day for eligible clients |

FAQ

Is KOHO or Neo better?

Since their exact plans and services differ, whether KOHO or Neo is the best fintech company for you depends on what you're looking for. That said, KOHO beats Neo in several of our direct-comparison categories, including best mobile app, credit cards, fees, and more.

Is Neo the same as KOHO?

No, Neo and KOHO are separate fintech groups that happen to offer similar products. Neo provides separate chequing and savings accounts, while KOHO offers a hybrid chequing/savings account. Both Canadian fintech companies also offer credit-building tools and investment opportunities.

What are the downsides of the Neo Card?

The standard Neo card is fairly basic. Although there's no annual fee, the welcome bonus is pretty small, and your rewards are capped – all of which limit the card's value. Neo's premium credit cards also have reward caps, which is disappointing given the high income requirements for these cards.

Is KOHO good in Canada?

KOHO is a solid option for using a hybrid chequing/savings account and building your credit score in Canada. Depending on what you're looking for to manage your finances, you can choose from 3 plans, which cost between $0 and $14.75 a month.

How do Neo vs. KOHO vs. Wealthsimple compare?

Each of these fintech groups is a popular alternative to traditional banks. Neo is best known for its range of credit cards and high cash back rates, while KOHO simplifies credit building and offers budgeting tools. Wealthsimple's strong suit is investments, but it also handles retirement accounts.

creditcardGenius is the only tool that compares 126+ features of 251 Canadian credit cards using math-based ratings and rankings that respond to your needs, instantly. Take our quiz and see which of Canada's 251 cards is for you.

GC:

GC:

Comments

Leave a comment

Required fields are marked with *. Your email address will not be published.