Best Prepaid Credit Card in Canada for 2026

Safe spending – and even some rewards – with top credit card alternatives.

The best prepaid credit card in Canada is the EQ Bank Card, followed by the Wealthsimple Prepaid Mastercard and KOHO Everything Mastercard.

These 3 cards top the charts for Genius Rating, a score given to every credit card in Canada based on a comparison of over 126 features.

| Prepaid credit card | Pros | Cons | |

|---|---|---|---|

| #1 | EQ Bank Card | * Earn up to 2.75% interest on your account balance * Earn 0.5% cash back * No annual or foreign exchange fees * No credit check needed | * Won’t build credit * No insurance included |

| #2 | Wealthsimple Prepaid Mastercard | * Earn up to 2.25% interest on your account balance * No annual or foreign exchange fees * Free Canada-wide ATM use | * No longer offers cash back * No insurance included |

| #3 | KOHO Everything Mastercard | * Up to 2% cash back on purchases * Earn 3.5% on your balance * No foreign exchange fees | * No insurance included |

Prepaid cards are a valuable alternative to traditional credit cards, offering opportunities for Canadian newcomers, students, individuals with low credit scores, and others. They won't and can't help build your credit, but you also don't have to worry about interest charges, annual fees, or credit checks.

Below, you'll find all the information you need on the top prepaid card options in Canada, broken down by their benefits, drawbacks, and key details.

Key Takeaways

- Prepaid credit cards are not credit products as you load the balance in advance of spending it.

- Prepaid credit cards have no income and credit score requirements – and most have no annual fee.

- The biggest downside to prepaid credit cards is the lack of rewards compared to standard credit cards.

Best prepaid credit cards in Canada

Our Gold award for the #1 prepaid card in Canada goes to the EQ Bank Card. Not only does this card have no annual fee, it also has no foreign transaction fees, making it a great prepaid card for travel. Cardholders can also benefit from earning interest on their account balance.

Our Silver award goes to the Wealthsimple Prepaid Mastercard, which offers many of the same features of the EQ Bank Card (including up to 2.25% interest on your account balance and no foreign currency exchange fees), also for no annual fee. However, this card no longer offers cash back.

Finally, our Bronze award goes to the KOHO Everything Mastercard, which offers a great selection of features (interest on your balance, cash back rewards) but falls behind the top two due to its annual fee and reduced (but not waived) foreign transaction fee.

Canada’s best prepaid card: EQ Bank Card

If you’re searching for a prepaid card, the EQ Bank Card is our top pick. On everyday purchases, the card earns 0.5% cash back, which, while not as impressive as a top cash-back card, is still strong for a card with no annual fee, no foreign transaction fees, and no credit check.

EQ also reimburses ATM fees within 10 business days, giving you easy access to cash on the go. This card also charges no foreign exchange fees and earns interest on your balance, making it an excellent travel credit card.

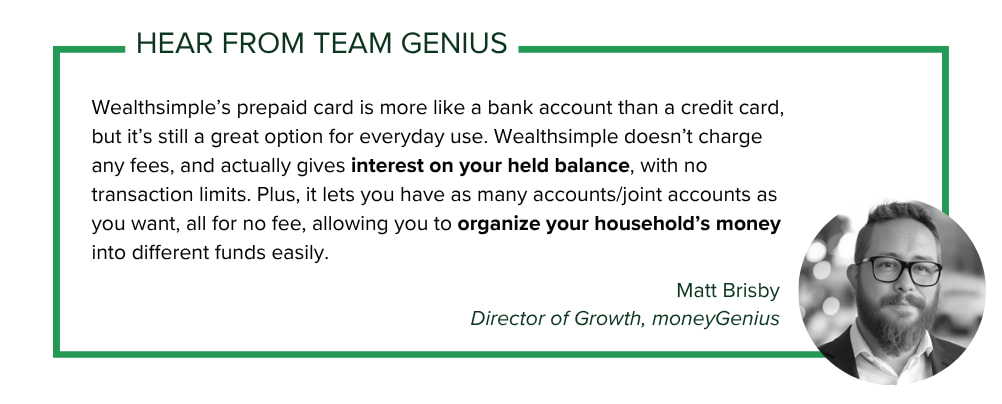

Silver award prepaid card: Wealthsimple Prepaid Mastercard

Frequent travellers might also appreciate the Wealthsimple Prepaid Mastercard. You won’t pay any foreign exchange fees or an annual fee to use the card.

The Wealthsimple Prepaid Mastercard used to offer 1% cash back on purchases, but this is no longer available.

However, you’ll earn up to 2.25% interest on your prepaid balance, depending on your Wealthsimple account type.

- Generation ($500k+ holdings) – 2.25% interest

- Premium ($100k+ holdings) – 1.75% interest

- Other – 1.25% interest

Bronze award prepaid card: KOHO Everything Mastercard

×1 Award winner

×1 Award winner  $100 GeniusCash + Up to 2% cash back on purchases + No foreign exchange fees.*

$100 GeniusCash + Up to 2% cash back on purchases + No foreign exchange fees.*

1x Award winner

1x Award winner

Among the KOHO Everything Mastercard’s many features is a 50% discount on the Koho Credit Building service (a $5 monthly savings). This monthly payment is reported to credit monitoring bureaus, which can help build your credit score over time. You’ll also get access to your credit score.

The (relatively) high fee for the KOHO Everything Mastercard might make you dismiss this KOHO card, but note that it’s charged out at $14.75 per month. This fee may be worthwhile, as it provides a hybrid bank account that earns interest on your balance and offers cash back.

You’ll also get better rewards with this card than other prepaid cards, earning up to 1.1% cash back.

Compare top prepaid credit cards by Genius Rating

To generate our Genius Ratings, we analyze 126 features of each credit card in 7 main categories. Then, we run the data through our algorithm to calculate a score out of five – our Genius Rating. We use a monthly spending estimate of $3,000 to make a fair comparison of reward value.

- Rewards (31%)

- Fees (20%)

- Insurance (16%)

- Perks (16%)

- Interest (7%)

- Acceptance (5%)

- Approval (5%)

Here’s how the top prepaid cards compare when arranged by Genius Rating:

×1 Award winner 1x Award winner

Learn more about our Genius Rating methodology.

How to choose the right prepaid card

As always, the best credit card will be one that suits your personal needs. This means finding a prepaid card that provides features like interest on your balance, cash back rewards, and a low (or non-existent) annual fee.

If you like to travel, pay close attention to the card’s foreign transaction fee, as some of the cards on our list waive this charge.

Rewards

While you might not earn as much as with a standard credit card, the best prepaid credit cards offer cash back on your purchases. No, the rewards won’t be as impressive as you’d find with a cash back credit card, but they still provide additional value that can really enhance the overall value of the prepaid card.

Both the EQ Bank Card and KOHO Everything Mastercard earn 0.5% on everyday purchases. However, the KOHO Everything Mastercard earns 2% on groceries, restaurants, and transportation, bumping its average return to 1.1%.

As mentioned, the Wealthsimple Prepaid Mastercard no longer earns cash back.

Tip: No matter what credit card you use, you could be earning bonus cash back on top of your card's rewards. Input your monthly spend in the GeniusCash app, and level up to earn real cash.

Fees

Many prepaid cards have no annual fees, and others offer a lower-tier, no-fee version. Some, however, always charge a fee. The KOHO Everything Mastercard, for example, charges a $177 annual fee, whereas the other cards do not.

To decide whether the KOHO Everything Mastercard’s fee is worth paying, consider how much you plan to spend on groceries, restaurants, and transportation, since this is where you’ll earn your bonus rewards.

With a typical monthly spend of $3000, you can expect approximately $396 in annual rewards from this card, offsetting its fee. However, if it’s not your go-to card, or you have lower monthly expenses, you may not make back your fee in rewards.

Both the EQ Bank Card and the Wealthsimple Prepaid Mastercard eliminate foreign currency exchange fees, a feature typically found only on versatile travel rewards credit cards. The KOHO Everything Mastercard doesn’t waive the foreign transaction fee; instead, it offers a reduced 1.5% fee on foreign currency purchases.

Perks

As with other products, prepaid cards typically offer fewer benefits than credit cards. The most impressive feature of some prepaid cards is the ability to earn interest on the funds in the account.

When it comes to interest, the EQ Bank Card comes out on top of the Wealthsimple Prepaid Mastercard. Even with $500,000 in Wealthsimple assets, you’ll earn more interest with EQ.

You’ll get the most interest from Koho, but remember to factor in the $177 annual fee.

Insurance

Since a prepaid card doesn’t charge interest, it can’t offer cardholders perks such as travel insurance, discounts, or roadside assistance. In fact, most prepaid cards lack even the most basic protections, such as extended warranty or purchase protection.

Interest rates

Since you load your card with money before you spend it, you’re not borrowing and will never have to worry about paying 20% or more in credit card interest, as you would with a standard card.

Acceptance

All of the best prepaid credit cards in Canada have high acceptance, so you can use them the same as a regular credit card.

Approval

One benefit of prepaid cards is that they eliminate many of the eligibility requirements that make credit cards difficult to obtain.

Unlike a credit card, prepaid cards don’t require a credit score or credit check to receive, nor do they require the income requirements that many banks screen for when applying.

This makes a prepaid card a great option for those without a credit history, those recovering from bankruptcy or other challenging financial events, or those who want a simple payment card linked to a deposit account.

How prepaid credit cards work

Instead of applying for credit and being offered a card with a credit limit, a prepaid credit card works a little differently.

What is a prepaid credit card?

Prepaid credit cards are still part of the Visa or Mastercard network, but you’ll deposit money into the account before using it. When you make a purchase, the merchant will pull money from the prepaid account.

- A prepaid credit card uses money that you’ve already put into an account – kind of like a debit card.

- A standard credit card doesn’t require you to fund the account first; the card issuer fronts the money, and you pay it back by your statement due date (or carry a balance and pay interest on the loan).

Think of it this way: You can't spend more on prepaid cards than what’s in your account. Since a prepaid card isn't a credit product, you won't need a credit check to get one, nor will your credit score be affected in any way. This makes a prepaid credit card a good option if you need to stick to a budget or have poor credit.

How to reload a prepaid credit card

Depending on your card type, you can reload it using your online banking portal or app by transferring funds directly. If you're using a card from an issuer other than your bank, you can use methods like:

- Direct debit

- e-Transfer

- Wire transfer

- Online bill payments

Pros and cons of prepaid credit cards

To help you decide if a prepaid credit card is right for you, consider the following.

Pros:

- No credit card interest: Since you load the card with money before you spend it, you’re not borrowing and will never have to worry about paying 20% or more in credit card interest.

- Earn rewards on purchases: While you might not earn as much as with a standard credit card, the best prepaid credit cards offer cash back on your purchases.

- (Usually) no annual fees: With one exception, prepaid cards have no annual fees – and you always have the option to opt for a lower-tier, no-fee version.

- No credit checks: A credit card issuer won’t pull your score for a credit check, and your prepaid card won’t appear on your credit file. This makes a prepaid card a strong option for someone with poor credit who might not otherwise qualify for a credit card.

Cons:

- Minimal rewards: If you’re hoping for great earn rates, you’ll be disappointed – these cards offer some rewards but very little in comparison to the best standard credit cards.

- Few to no perks: Since a prepaid card doesn’t charge interest, it can’t reward cardholders with perks or benefits like travel insurance, discounts, or roadside assistance.

- Doesn’t help credit score: Since they're not credit products, prepaid credit cards won't help you build a credit history or improve your credit score. To do that, you’ll need a secured credit card.

- Won’t be accepted everywhere: Some retailers and service providers may not accept prepaid credit cards as a form of payment.

Credit card expert Patrick Sojka notes that prepaid credit cards aren’t always the right choice. "There are places that will use prepaid cards, but for some purchases, you don't want to use prepaid cards," he shares. “They are not as secure as regular credit cards."

Not all prepaid cards offer deposit insurance or coverage for fraudulent transactions. This can make certain prepaid credit cards less secure and is one reason some service providers don’t accept them.

Why use a prepaid credit card?

Prepaid cards may not be "real" credit products, but there are many times when using a prepaid credit card is a great idea. Here are some common reasons you may want to reach for one:

- You’re trying to budget or watch your spending: With prepaid cards, there’s no danger of spending more than you have (or have budgeted). You’re in control by loading money onto the card, which essentially becomes your spending limit.

- You’re travelling and don’t want to carry cash: You’ll get peace of mind knowing you’re not carrying large amounts of cash. Plus, top prepaid cards like the EQ Bank Card and Wealthsimple Prepaid Mastercard don’t charge FX fees, which are typically 2.5%.

- You’re young and learning to be financially independent: Prepaid cards are great tools for teaching financial responsibility without the risk of going into debt. Parents can give their teens or young adult children prepaid cards to help them manage their budget.

- You frequently shop online: When you shop online, there’s always the risk that your credit card or bank account information could be stolen. By using a prepaid card, you reduce the risk of fraud because thieves can’t run up a debt using your information.

- You have poor or no credit history: If you can’t qualify for a credit card but want a way to pay for things without cash, prepaid cards are a good option. They don’t build credit, but they can make paying for things easier.

Alternatives to prepaid credit cards

If prepaid cards don’t sound like the right product for you, you’ve got other choices:

- Use a debit card. Like prepaid cards, very few debit cards offer rewards on purchases – but you won’t be able to rack up a balance or overspend.

- Use a secured credit card. If you need to build credit, you can apply for a secured card. You’ll provide a deposit that will be your credit limit, which means you’ll only be able to spend what you can afford. Make your payments on time and in full, and you’ll see improvements to your credit score.

Read more: Best Secured Credit Cards for 2026

FAQ

Which prepaid credit card is best?

The EQ Bank Card is the best prepaid card on the market right now. Cardholders earn interest on their balance, pay no annual fee, and incur no foreign exchange fees, all while enjoying free access to ATMs across Canada.

How long do prepaid credit cards last?

The card's validity period varies, but it will always be specified on the card. Even if your prepaid card expires, you can retrieve any money left on it, though there may be transfer fees.

Does a prepaid card hurt your credit?

No, unlike a secured credit card, your prepaid card isn’t tied to your credit score. On the other hand, using your prepaid card responsibly won’t improve your credit score, which isn’t great news if you’re trying to build credit.

How much does it cost to activate a prepaid Visa card in Canada?

The cost depends on the card itself and the issuer. The best way to check the cost is to read the card’s terms and conditions before buying it. Activation fees are often a percentage of the card's balance.

How to get a prepaid credit card in Canada

Before you get a prepaid credit card, you’ll have to meet two criteria:

- Age of majority in your province or territory

- Resident of Canada

That’s it! Prepaid credit card issuers don’t consider your income or credit score to qualify you for a card. As long as you load money to your card in advance, you’re good to go.

What happens when you cancel a prepaid card?

As the Financial Consumer Agency of Canada notes, you typically can’t cancel a prepaid card because you’ve already deposited funds into the account. Your best option is to use it until the balance is zero. Some prepaid card issuers might be willing to cancel your card, but they may deduct a fee from the balance before returning the funds to you.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.