Whether you’re applying for new credit or trying to see where you stand financially, you’ve probably come across the term debt-to-income ratio. Simply put, your debt-to-income ratio (DTI) in Canada is the ratio of your monthly debts to your monthly income.

You’ll see it shown as a percentage. The higher the percentage, the more debts and financial obligations you have. The lower that number, the more likely you are to be approved for loans and new credit. Let’s dive into what’s included in your DTI.

Key Takeaways

- Debt-to-income ratio is the ratio of your monthly debt to your income shown as a percentage.

- Canadians’ household service debt, which includes all monthly housing costs, has risen to 14.4%.

- Canadians owe an average of $1.75 for every $1 they have in income.

Never miss an amazing deal again + get our bonus 250+ page eBook for FREE. Join 50,000 other Canadians who receive our weekly newsletter – learn more.

What is debt-to-income ratio?

Your debt-to-income ratio (DTI) is the ratio of your total monthly debt compared to your income. It’s usually shown as a percentage and can help lenders gauge how comfortably you could handle new debt.

According to TransUnion, creditors like to see debt-to-income ratios of 35%. However, if your DTI is high, it’s not necessarily a bad thing. This ratio can be skewed if you’ve just made a large purchase, like a mortgage. Your DTI might appear high, but it doesn’t necessarily reflect that you can’t handle the debt you’ve taken on.

Calculating your debt-to-income ratio

You’re probably wondering where you stand with your debt and income. You can calculate it pretty easily (more on that in the following example), or you could use a simple online calculator.

All you’re figuring is your monthly debt payments divided by your monthly income. Since DTI is usually expressed as a percentage, you’ll multiply your answer by 100. Here’s how it looks as a formula:

(Total monthly debt payments / gross monthly income) x 100 = household debt ratio

Your debt payments include:

- Mortgage payments, as well as property taxes and insurance

- Auto loan payments

- Minimum monthly credit card bills

- Personal or student loans

- Child support and alimony payments

An example of calculating your debt-to-income ratio

To calculate your own DTI, take a look at this example. Let’s imagine you have a monthly household income of $5,000 before taxes (your gross income).

Here are your monthly debts:

- Mortgage, including taxes and insurance: $1,000

- Car payment: $400

- Minimum credit card payments: $50

That's a total of $1,450 in monthly debt. So, you’d take your debts divided by income before taxes to get your DTI:

($1,450 / $5,000) x 100 = 29%

Canada's household debt-to-income ratio average

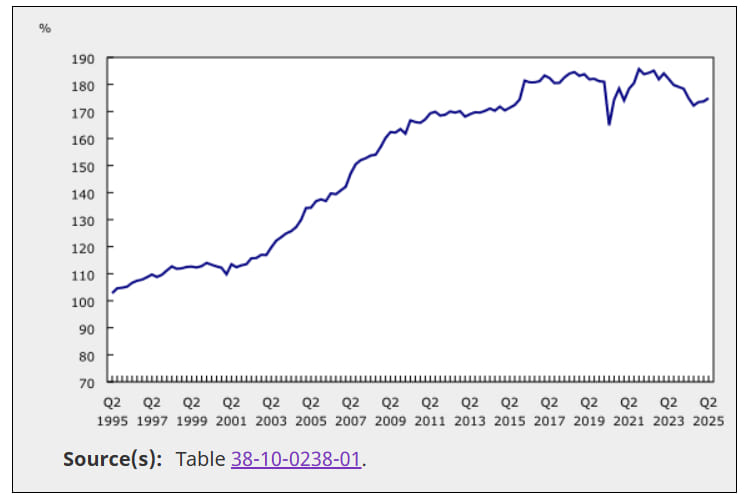

You’re not alone in carrying debt. As of Quarter 2 in 2025, the average household debt-to-income ratio stood at 174.9%. This means that for every $1 of disposable income Canadians brought in, they owed $1.75 to creditors.

Here's what this ratio has looked like since 1995.

Source: Statistics Canada

As you can see, although it’s not the highest it’s ever been, the debt-to-income ratio remains elevated.

Trends in the debt ratio this year

What has happened to the debt ratio so far this year? Several years ago, we saw that the debt ratio was higher than it is now. However, the ratio has been steadily increasing since Q3 of 2024, suggesting that Canadians are dealing with more debt.

Statistics Canada has yet to release third-quarter data for 2025.

Should you care about Canada's rising debt-to-income ratio?

At this time, no, the rising DTF shouldn't worry you. It has been steadily rising for 30 years now. And, as you can see in the graph above, it has been relatively level for the last five years.

Keep in mind, however, that all this does is reflect the total amount that all Canadians owe, versus the income we collectively have at our disposal after taxes.

On an individual level, this isn't the number you should be worrying about unless you’re applying for a mortgage or new credit. The real number you need to consider is your household service ratio.

This ratio measures your ability to pay your debts. It’s basically your debt-to-income ratio, but it looks at all of your household debts and expenses, so lenders get a better idea of your finances.

Improving your debt-to-income ratio

There are essentially two ways to improve your DTI: reduce your debt or increase your income. Here are ways to do both.

Pick up a side hustle

Lean into your hobbies and start a job that you can do on the side. Or, try your hand at gig work like a rideshare or food delivery service.

Getting a side hustle, such as freelancing, is one way to earn more money.

Eliminate your credit card debt

Your monthly credit card debt is a straightforward one to tackle. If you have even a small amount of credit card debt, you're probably paying around 20% interest on it (which isn’t great).

Instead, here are a couple of credit cards that have great balance transfer offers you can use to significantly reduce your interest payments while you work on eliminating that debt.

| Credit Card | Balance Transfer Offer | Annual Fee, Income Requirements | Apply Now |

|---|---|---|---|

| MBNA True Line® Mastercard® | 0% for 12 months | * $0 * None | Apply Now |

| BMO CashBack® Mastercard®* | 0.99% for 9 months | * $0 * None | Apply Now |

| BMO Preferred Rate Mastercard®* | 0.99% for 9 months | * $29 * None | Apply Now |

Consider refinancing your mortgage

Refinancing your mortgage can be more difficult if you're in the middle of your term, but it can be worth exploring if there are lower interest rates you can take advantage of.

Generally, if interest rates have fallen by at least a percentage point since you took out the mortgage, you could benefit from refinancing, even though you’ll have to pay for the process and the new loan.

But with a lower interest rate, not only will your monthly payments go down, but more of what you pay will go towards paying the principal. It’s a matter of doing the math and deciding whether it’s worth it.

Don’t add more debt

You’ve heard it before, but making a budget and sticking to it is one of the best ways to be accountable for your money. Start tracking every dollar you spend so you can see where your money is going and where you can cut back.

By freeing up budget funds, you can allocate more toward your debt.

Explaining household debt service ratio

In many ways, the household debt service ratio is a better indicator of your financial situation. It’s the same formula as DTI, but it uses disposable income (also called net income) instead of gross income. If you use an online calculator, it will ask for things like:

- Monthly mortgage or rent payment

- Monthly heating expenses

- Monthly property taxes

- Credit card payments

- Loans or lines of credit

- Car payment or lease

Is there a magic threshold you want this number to be under? Generally, you'll want to keep your debt service ratio below 39% (which lenders typically use).

In 2025, the average debt service ratio in Canada remained steady at around 14.41%. Meaning, most Canadians are well within their means to pay what they owe.

Why lenders care about this number

Lenders care about this number because it gives them a relatively accurate idea of your ability to pay your debt. If your debt service ratio number gets too high, you're taking on more debt than you can afford.

And since this calculation uses your disposable income, it shows lenders if you’re cash-strapped after paying monthly housing debts.

FAQ

What is the average debt-to-income ratio in Canada?

The average debt-to-income ratio – also referred to as the DTI ratio – in Canada stood at 174.9% as of Quarter 3 in 2025 (rates for Quarter 4 have not yet been released). As you can see on the chart above, it’s hovered around 180% since 2016, briefly rising and falling slightly.

What is a good household debt-to-income ratio?

Ideally, your household debt service ratio should be no more than 39%, though creditors prefer a ratio of 35% or lower. You can determine your own DTI ratio with this formula: (Total monthly debt payments / gross monthly income) x 100 = household debt ratio.

What does "household debt service ratio" mean?

The household debt service ratio looks at your monthly debt payments — including both interest and principal — and divides them by your monthly disposable income. This helps determine whether you can comfortably take on more debt. A high ratio means you have less wiggle room if your financial situation changes.

Where can I find a debt-to-income calculator in Canada?

There are plenty of debt-to-income ratio calculators online. It will prompt you to enter specific debts, such as your mortgage, rent, or child support payments, as well as your monthly income. However, you can determine this ratio for yourself with this formula: (Total monthly debt payments / gross monthly income) x 100 = household debt ratio.

How much debt does the average Canadian have?

Although it varies widely by age, overall, the average Canadian has $22,147 in debt (as of Q2 2025) – an increase of 2.3% over the same quarter of the previous year. The province with the highest level of debt is Newfoundland and Labrador, with an average of $25,174.

creditcardGenius is the only tool that compares 126+ features of 257 Canadian credit cards using math-based ratings and rankings that respond to your needs, instantly. Take our quiz and see which of Canada's 257 cards is for you.

GC:

GC:

Comments

Leave a comment

Required fields are marked with *. Your email address will not be published.