Best No Foreign Exchange Fee Credit Cards in Canada for 2026

Save on the standard 2.5% currency exchange fee on non-CAD purchases.

The best foreign exchange credit card in Canada is the Scotiabank Gold American Express® Card, followed by the Scotiabank American Express® Platinum Card and Scotiabank Passport Visa Infinite+ Card. These cards waive the usual 2.5% foreign exchange fee, so cardholders can easily use their cards abroad without incurring additional charges for each transaction.

| Credit card | Foreign exchange fee | Annual fee | Average earn rate | |

|---|---|---|---|---|

| #1 | Scotiabank Gold American Express Card | 0% | $120 | 2.45% |

| #2 | Scotiabank American Express Platinum Card | 0% | $399 | 2% |

| #3 | Scotiabank Passport Visa Infinite+ Card | 0% | $150 | 1.35% |

These credit cards feature the best that travel cards have to offer: generous insurance coverage, large welcome offers, and sometimes complimentary airport lounge access. Saving on those pesky foreign exchange fees is the icing on the cake for frequent travellers looking to maximize their spending.

This article offers in-depth reviews of Canada's top foreign exchange credit cards, provides tips on how to choose the best card for your needs, and more.

Key Takeaways

- The Scotiabank Gold American Express Card is the best foreign exchange fee credit card for Canadians.

- The EQ Bank Card is a unique prepaid credit card that doesn't charge foreign exchange fees.

- Most no-FX fee credit cards are travel cards, so when choosing one, look to see which features are included to make travel more valuable and convenient.

Best foreign exchange credit cards in Canada

Our Gold award for the best foreign exchange credit card in Canada goes to the Scotiabank Gold American Express Card , a card that waives foreign transaction fees, provides membership to the Priority Pass airport lounge program, and earns up popular Scene+ points at a high rate.

Our Silver award goes to the premium Scotiabank American Express Platinum Card, thanks to its 10 free lounge passes, extensive travel and medical insurance, and surprisingly low interest rates for purchases, cash advances, and balance transfers.

And our Bronze award goes to the Scotiabank Passport Visa Infinite+ Card, a card that earns generous points on travel and groceries, six free lounge visits via the Visa Airport Companion program, and complimentary Preferred Plus Membership through Avis car rentals.

However, you don’t need to pay a steep annual fee to enjoy no foreign transaction (FX) fees. The Home Trust Preferred Visa, for example, charges no fee yet remains an excellent option for avoiding FX charges. In fact, you don’t even need a true credit card, as the EQ Bank Card is a prepaid credit card that doesn't charge FX fees, making it a convenient and worthwhile choice for students and many others.

The #1 foreign exchange card in Canada: Scotiabank Gold American Express® Card

×3 Award winner

×3 Award winner  $75 GeniusCash + Up to 50,000 bonus points + No foreign exchange fees.*

$75 GeniusCash + Up to 50,000 bonus points + No foreign exchange fees.*

3x Award winner

3x Award winner

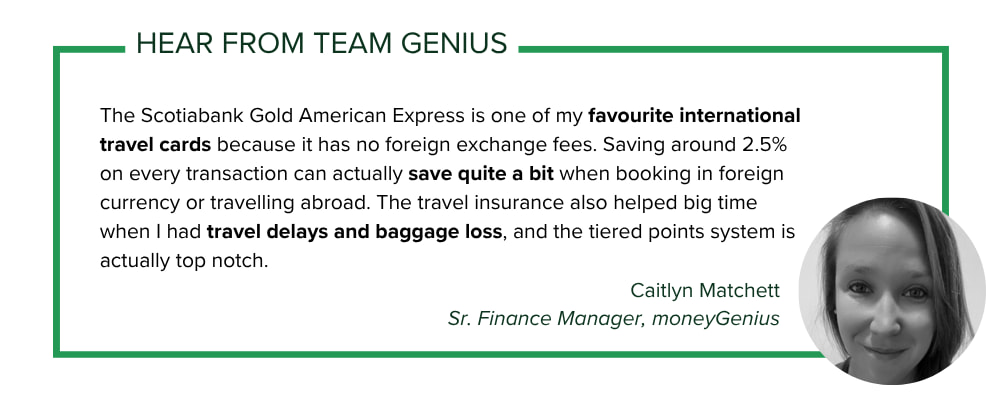

Our top pick for the best foreign exchange credit card is the Scotiabank Gold American Express® Card. In addition to saving on all foreign currency transactions, you get a very competitive earn rate of 2.45% for versatile Scene+ points, and you kick off your rewards with a sweet 50,000-point sign-up bonus that's worth $350.

Anyone looking for a travel card will likely be concerned with its insurance package, and this card doesn't disappoint. It offers 12 types of coverage, including emergency medical services for an impressive 25 days (3 days for those over age 65), to a max of $1 million. Mobile device coverage is also included – a rare addition. The total value of included insurance is around $475.

The Scotiabank Gold American Express Card is surprisingly accessible, with personal income requirements of just $12,000 and no household income requirements at all. Plus, the card's reasonable $120 annual fee is waived for the first year.

Silver award for best foreign exchange card in Canada: Scotiabank American Express® Platinum Card

The Scotiabank American Express® Platinum Card, the Scotia Gold Amex's pricier sibling, also waives foreign transaction fees but increases the travel perks even further. Users have ten complimentary airport lounge passes through Priority Pass, and are eligible for four more free passes when a supplementary card is added. Plus, it comes with 12 types of insurance, including 31 days of emergency medical coverage – ten days for those over age 65 – to a maximum of $2 million in coverage.

In terms of rewards, this Platinum card earns 2x on all purchases and comes with a huge welcome offer of 60000, 20000, 20000 points, valued at up to $1,000. That’s enough to cover the $399 annual fee for two years.

Finally, the Scotiabank American Express Platinum Card prioritizes low interest rates – not just promotional rates, either. Its regular purchase, balance transfer, and cash advance rate is set at a very reasonable 9.99%, one of the lowest in all of Canada.

Bronze award for best foreign exchange card in Canada: Scotiabank Passport Visa Infinite+ Card

×1 Award winner

1x Award winner

1x Award winner

Another solid product from one of Canada's biggest banks, the Scotiabank Passport Visa Infinite+ Card is a competitive option for a no-FX fee credit card. You’ll get a solid 1.35% average return on your spending with the following rewards:

- 3 Scene+ points per $1 spent at Sobeys, Safeway, FreshCo and more

- 2 Scene+ points per $1 spent on groceries, restaurants, entertainment, and daily transit

- 1 Scene+ point per $1 on all other purchases

You can add one supplementary card/user for free, too, which can help boost your earnings.

Yes, the card has an annual fee, but it's a reasonable $150. For that, you'll enjoy perks like 11 types of insurance (including 25 days of emergency medical coverage) and Visa Airport Companion Program membership, which provides six free passes each year.

Best foreign exchange card with no annual fee: Home Trust Preferred Visa

If you want a no-fee card and a Scotiabank alternative, the Home Trust Preferred Visa is a top choice. It provides a straightforward 1% cash back on all purchases, aside from those made in foreign currencies, with no spending cap.

Because it's a Preferred card, using this card to book a hotel stay guarantees that a room will be held for you, even if you're late.

There aren't nearly as many perks or freebies with the Home Trust Preferred Visa as with the other no-FX cards on our list, but it's still a valuable choice for travellers who want to save on annual fees.

Best prepaid foreign exchange card: EQ Bank Card

Another no-fee option for bypassing foreign exchange fees is the EQ Bank Card, which is also the best prepaid credit card in Canada. Because it's a prepaid card, there are no credit requirements, so no credit check is necessary. This makes it a prime option for students, those with low credit, or those trying to avoid falling into credit card debt.

At 0.5%, the cash back earn rate is low, but it's not nothing. And the money you deposit into the associated EQ Bank account earns a generous 2.75% interest.

True, it doesn't have the insurance or benefits that come with other premium foreign exchange travel cards on our list, but the EQ Bank Card's unique features make it a worthwhile option for many Canadians.

Compare all top foreign exchange credit cards by Genius Rating

Our system scores all 250 credit cards we review using an unbiased, math-based algorithm that assigns each card a Genius Rating out of 5 stars. We regularly review and update our weighted scoring methodology to ensure transparency and accuracy.

×3 Award winner 3x Award winner ×1 Award winner 1x Award winner

The Genius Rating methodology

To identify the best foreign exchange credit cards in Canada, we examine over 126 credit card features in seven main categories, weighting them as follows:

- Rewards: 31%

- Fees: 20%

- Insurance: 16%

- Perks: 16%

- Interest: 7%

- Acceptance: 5%

- Approval: 5%

Learn more about our Genius Rating methodology

How to choose the right foreign exchange credit card

The right foreign exchange credit card will have a high earn rate for valuable travel rewards, include standout insurance packages, and, of course, not charge any FX fees.

There will be personal preferences for you to consider as well. You might want to avoid fees altogether and, therefore, should look for cards with no annual fees. Or you might want to keep costs down with a low-interest card.

The following sections break down the factors that go into choosing a foreign exchange credit card, offering information and advice to help you find the right product for your needs.

Rewards

Since all the top foreign transaction cards are similar travel cards, choosing one requires closely examining details about earning and redeeming rewards. You'll want a card that earns in the categories where you spend the most, like groceries, restaurants, gas, etc.

Naturally, it should be a rewards program that's valuable to you, too. Earning gas station points at an exceptional rate isn't going to help you at all if you cycle everywhere.

The top three cards on our list all earn Scene+ points, but each earns different amounts in different categories. Here are some highlights:

- The Scotiabank Gold American Express Card card has the best earn rate for groceries: 5 Scene+ points per $1 spent – this goes up to 6 points per $1 if you shop at Sobeys or Safeway stores

- The Scotiabank American Express Platinum Card has a very convenient flat earn rate of 2 Scene+ points per $1 spent on all purchases.

- The Home Trust Preferred Visa card also earns a flat rate, but this one gives cash back: 1% back on all purchases.

This is how the average earn rates of the top five foreign exchange cards compare:

Tip: No matter what credit card you use, you could be earning bonus cash back on top of your card's rewards. Input your monthly spend in the GeniusCash app, and level up to earn real cash.

Fees

The best travel cards waive one of the most frustrating charges: the foreign transaction fee. Most banks charge a foreign transaction fee of 2.5%, meaning if you were to spend $1,000 abroad, you’d be hit with a $25 fee. Considering all the expenses people encounter while travelling, these fees can and will add up significantly.

The other major fee to consider is the annual fee. Some cards, like the Scotiabank American Express Platinum Card, charge steep annual fees ($399), while others, like the Home Trust Preferred Visa, don't charge one at all. It’s essential to weigh the rewards and ongoing value of a card against its fee.

To be fair to the Scotiabank American Express Platinum Card, it also has low interest rates, which makes our case: high annual fees can easily be outweighed by other factors.

Insurance

As with co-branded airline cards and the best travel cards, many no-FX fee credit cards offer exceptional insurance coverage. It's a popular and highly cost-effective feature that sets these cards apart from other types.

Aside from the EQ Bank Card, a prepaid card with (unsurprisingly) no insurance, here's a look at the insurance packages offered by the best foreign exchange cards:

- Scotiabank Gold American Express Card: 12 types of coverage

- Scotiabank American Express Platinum Card: 12 types of coverage

- Scotiabank Passport Visa Infinite+ Card: 11 types of coverage

- Home Trust Preferred Visa: 1 type of coverage

And here's how the total values of those insurance packages compare:

Perks

Credit card perks are perhaps the most exciting part of a travel credit card – in fact, the lack of a foreign exchange fee is in itself a significant benefit. When choosing between these cards, you should of course consider which offers the most financially rewarding perks, but also which ones are useful for you.

For instance, the Scotiabank Gold American Express Card provides ten free airport lounge passes, and the Scotiabank American Express Platinum Card provides six, but gives you another four when you add a supplemental card to your account. If you don't have anyone to add as another user, but you still want those ten free passes, the Scotiabank Gold American Express Card is a more logical choice.

Speaking of adding supplemental cards, that is an excellent perk in itself. Cards like the Scotiabank Passport Visa Infinite+ Card and Home Trust Preferred Visa allow you to add a user for free, while other charge cards charge significant fees for this.

Interest rates

If low interest is important to you, the best no-FX fee card is the Scotiabank American Express Platinum Card. It has a purchase, cash advance, and balance transfer rate set at 9.99%.

While the EQ Bank Card, as a prepaid card, doesn't have interest rates, the rest of the best foreign exchange credit cards do. For a big picture for comparison, this chart depicts the interest rates for the other four top cards in this category:

Acceptance

Since we're discussing travel cards, it's important to note that Visa and Mastercard have excellent acceptance rates across the globe. Historically, American Express hasn't been quite as well accepted on an international level, but the company continues to improve on this.

In fact, Forbes recently reported that Amex is accepted in 200 countries and territories, virtually matching the global reach of Visa and Mastercard.

We mention this since three of the five top foreign exchange credit cards on our list are American Express cards, and people are sometimes concerned about Amex acceptance. Overall, users shouldn't have any problems using their Amex foreign exchange cards at home or abroad.

Approval

Eligibility requirements for foreign exchange cards vary significantly. More premium options, like the Scotiabank American Express Platinum Card, require high credit scores (approximately 725+), while others, like the no-fee Home Trust Preferred Visa, require more middle-of-the-road scores (approximately 560-659).

Income requirements vary, too. For example, the Scotiabank Gold American Express Card and Scotiabank American Express Platinum Card expect a personal income of at least $12,000, and the EQ Bank Card, as a prepaid card, doesn't have any income requirements at all. Meanwhile, the Scotiabank Passport Visa Infinite+ Card requires either $60,000 in personal or $100,000 household income

These income and credit score ranges mean that many Canadians are eligible for at least one of our top five foreign exchange credit cards.

What is a no foreign transaction fee credit card?

A foreign exchange credit card – also called a no-foreign exchange fee card – is one that doesn't charge extra when you make purchases in a foreign currency. Most credit cards add a foreign transaction fee of 2.5% to 3% on top of international purchases, but no-FX fee cards waive this charge entirely.

For instance, if you purchase in a currency other than Canadian dollars, your card issuer converts the transaction into Canadian dollars at the credit card network's exchange rate. If you have an Amex card, they’ll first convert your purchase into U.S. dollars and then into Canadian dollars.

This process can be costly for the card issuer, so most charge an additional exchange rate markup, usually around 2.5% on top of the total transaction. This is the foreign transaction fee.

However, cards with no foreign transaction fees don’t do this, making them one of the best ways to get the most value for non-CAD purchases.

No foreign transaction fee vs. a U.S. dollar credit card

No foreign transaction fee cards are simply cards that don’t charge you when they convert your foreign purchases into Canadian dollars. But if you frequently make purchases in U.S. dollars, using a U.S. dollar credit card is another viable option.

With these credit cards, all transactions are processed in U.S. dollars, so when you pay your credit card bill, it must also be done in U.S. dollars. You won’t incur any currency conversion fees for U.S. dollars transactions with these cards, but you'll need a source of U.S. funds to pay your credit card bill.

Is a credit card with no FX fees worth it?

A credit card with no foreign exchange fees can definitely be worth it for careful users. If you’re paying an annual fee and not using the card very much, you might be better off with a standard credit card, even if it does charge FX fees.

On the other hand, if you frequently travel outside of the country or make frequent purchases from international websites, the savings add up.

Think about it – if you regularly travel abroad for work or pleasure, you’re probably using your card for accommodations, transit, dining out, buying groceries, and odds and ends. If you’re saving 2.5% on each transaction, a no-FX-fee card is probably worth it.

FAQ

Which credit cards do not charge a foreign transaction fee?

Several issuers offer credit cards that don’t charge foreign transaction fees, including Scotiabank, Home Trust, and EQ Bank. The best foreign exchange credit cards are the Scotiabank Gold American Express Card, Scotiabank American Express Platinum Card, and Scotiabank Passport Visa Infinite+ Card.

Which Canadian credit card is best for international travel?

The best credit card for international travel is the Scotiabank Gold American Express Card, primarily because it doesn't charge foreign exchange fees yet still offers premium travel perks. While the overall best travel card for Canadians is the American Express Cobalt Card, this card does charge FX fees, so be wary.

How do I avoid a 3% foreign transaction fee?

The best way to avoid any foreign transaction fee is to use a no-FX-fee credit card. Yes, there is a specific class of credit cards that doesn't charge these fees, and the best of the bunch is the Scotiabank Gold American Express Card. Alternatively, you can avoid FX charges by using a prepaid card like the EQ Bank Card.

Which TD card has no foreign transaction fee?

The TD U.S. Dollar Visa Card doesn’t charge a foreign transaction fee, but it charges an annual fee and doesn’t offer any rewards. Keep in mind that this card only works for purchases in U.S. dollars, not any other international currency. You’ll also need a U.S. dollar bank account to pay the credit card bill.

How is the exchange rate determined on my credit card?

Credit card networks each use different methods to determine exchange rates, which they update daily based on global currency markets. Once these rates are established, card issuers typically add a foreign transaction fee – usually 2.5% to 3% – to cover costs. No-FX fee cards remove this surcharge, saving you money on international purchases.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.