Best Rogers Credit Cards in Canada for 2026

An unbiased comparison of every top Rogers card in Canada

Rogers keeps its credit card lineup small, but mighty. The best Rogers credit card is the Rogers Red World Elite® Mastercard, having a slight edge over the Rogers Red Mastercard thanks to its sweet World Elite perks. Rogers customers looking for luxury perks may also want to consider the new Rogers Red World Legend™ Mastercard.

If you're a Fido, Rogers, Comwave, or Shaw customer, a credit card from Rogers Bank can be very valuable. Not only do these credit cards not charge any annual fees, but users can earn up to 2% cash back on purchases, bonus cash back, and free roaming days.

This article reviews Rogers credit card benefits, discusses their pros and cons, points out how Rogers makes it easier for newcomers to qualify for credit, and more.

Key Takeaways

- The best Rogers credit card is the Rogers Red World Elite Mastercard.

- Existing Fido, Rogers, Shaw, and Comwave customers get up to 3% cash back on purchases made in USD, 2% cash back on purchases in CAD, plus a 1.5x bonus when redeeming cash back for other company services.

- Rogers offers special services for newcomers to Canada, making it a bit easier to establish and build credit.

Best Rogers credit cards

| Category | Card name | Annual fee | Income requirements | Rewards | Welcome bonus | Learn more |

|---|---|---|---|---|---|---|

| Best for everyday value | Rogers Red World Elite Mastercard | $0 | * $80,000 personal * $150,000 household | * Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw * Earn 3% cash back on all eligible purchases made in U.S. dollars * Otherwise, earn 1.5% cash back on eligible non-U.S. dollar purchases | None | Learn more |

| Best no-fee card | Rogers Red Mastercard | $0 | * None | * Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw * Earn 2% cash back on all eligible purchases made in U.S. dollars * Otherwise, earn 1% cash back on eligible non-U.S. dollar purchases | None | Learn more |

| Best for luxury perks | Rogers Red World Legend Mastercard | $495 | * $150,000 personal * $200,000 household | * Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw * Earn 1.5% cash back on eligible non-U.S. dollar purchases | Learn more |

The best overall Rogers credit card: Rogers Red World Elite® Mastercard

Rewards:

- Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw

- Earn 3% cash back on all eligible purchases made in U.S. dollars

- Otherwise, earn 1.5% cash back on eligible non-U.S. dollar purchases

The best Rogers credit card is easily the Rogers Red World Elite Mastercard. Few cash back credit cards collect more than 1% across every purchase category, and even fewer offer World Elite Mastercard perks for free – but this one offers this and more. These perks include access to exclusive events, overseas cash back rewards, and a complimentary DragonPass membership, which lets you access 1,400+ airport lounges for $32 USD per visit.

Cardholders can redeem their cash back at any time, which isn't an especially common feature. Add in the lack of an annual fee, and this card offers excellent value and impressive convenience.

Pros:

- 6 types of insurance

- World Elite Mastercard perks

- Bonus cash back for Rogers, Fido, Comwave, and Shaw customers

- 5 free Roam Like Home days

- Redeem cash back on demand

Cons:

- 2.5% foreign transaction fee

- High income requirements

- Less travel insurance than other premium credit cards

Rogers' runner-up credit card: Rogers Red Mastercard

Rewards:

- Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw

- Earn 2% cash back on all eligible purchases made in U.S. dollars

- Otherwise, earn 1% cash back on eligible non-U.S. dollar purchases

The Rogers Red Mastercard offers slightly lower rewards than our first choice, but there are no income requirements and no annual fee either. Rogers, Fido, Comwave, and Shaw clients earn extra cash back, plus even more when said cash back is redeemed as statement credits for their respective services.

Cardholders also get 5 Roam Like Home days each year at no cost. This means you can use your phone in up to 185 different countries around the world and not pay a cent in roaming fees.

Pros:

- Bonus cash back for Rogers, Fido, Comwave, and Shaw customers

- No annual fee

- No income requirements

- 5 free Roam Like Home days

- Redeem cash back on demand

Cons:

- Mediocre rewards for non-Rogers customers

- No insurance

Best premium Rogers credit card: Rogers Red World Legend™ Mastercard

- Earn 2% cash back on all eligible non-U.S. dollar purchases if you have 1 qualifying service with Rogers, Fido, Comwave, or Shaw

- Earn 1.5% cash back on eligible non-U.S. dollar purchases

Mastercard has a new premium credit card tier, and Rogers is currently its only card issuer. The sleek, metal Rogers Red World Legend Mastercard is harder to qualify for, but you'll get the most luxurious benefits of any Rogers credit card.

Enjoy no foreign exchange fees when travelling abroad while earning 2% cash back on all eligible purchases around the world. You'll also get a 1.5x bonus if you redeem your cash back for Rogers services.

If the card's hefty annual fee puts you off, consider that you'll get a $200 Rogers entertainment credit every year, along with airport lounge access through Mastercard Travel Pass (along with 6 Plaza Premium Lounge passes per year).

Pros:

- 11 types of insurance

- World Legend Mastercard perks

- Soho friends account

- 10 free Roam Like Home days

- Access to Avis President's Club

Cons:

- High income requirements

- Steep annual fee

Compare all top Rogers credit cards by Genius Rating

Even though Rogers doesn't issue many credit cards, we use an unbiased algorithm to compare all the available cards. Our Genius Rating is regularly revised and audited, so you know we're showing evidence-based recommendations that are transparent and accurate.

Here's how Rogers credit cards compare when arranged by Genius Rating:

This credit card comparison table displays our default Genius Rating, which applies our standard weight to all 7 of our scoring categories (rewards, fees, insurance, interest, perks, approval, and acceptance). The ratings displayed for individual credit cards are weighted based on what each card does best.

Learn more about our Genius Rating methodology

Who should consider a Rogers credit card?

With cash back credit cards, Rogers could be a good choice for almost anyone – but some people might benefit more than others:

- Rogers, Fido, Shaw, or Comwave customers: If you have an eligible service with Rogers, Fido, or Shaw, you can earn 2% unlimited cash back on all eligible purchases.

- U.S. shoppers: The Rogers Red World Elite Mastercard earns you 3% cash back on USD purchases, making it a rewarding option for frequent cross-border and/or online shoppers.

- Frequent travellers: The basic and World Elite Mastercards give 5 Roam Like Home days per year and the Rogers Red World Legend Mastercard gives a generous 10 days per year, which allows you to travel abroad with your mobile plan for no extra cost in up to 185 international destinations.

- Budget-conscious consumers: 2 Rogers credit cards have no annual fees or annual spending requirements, which makes them ideal if you want to minimize additional costs while maximizing your rewards.

How to make the most out of your Rogers credit card

Rogers credit cards are fairly straightforward, but there are a few strategies you can use to ensure you're maximizing their value:

- Link your Rogers, Fido, Shaw, or Comwave account: To earn 2% unlimited cash back on all eligible purchases, ensure your Rogers credit card is linked to your Rogers, Fido, Shaw, or Comwave postpaid account. If you don't and you have the basic or World Elite Mastercard, your earn rate drops to 1% or 1.5% on non-U.S. dollar purchases, and you miss out on other perks, like the Roam Like Home days.

- Earn cash back for Rogers services: When you redeem points for Rogers, Fido, Shaw, or Comwave purchases, you'll get 1.5x cash back.

- Use Roam Like Home benefits: Enjoy 5 to 10 free roaming days every year when you travel outside Canada – a $90 to $180 annual savings.

- Monitor your rewards with the Rogers banking app: Set up app alerts so you don't miss bonus opportunities. You can also use the app to manage your account and redeem rewards.

Rogers services for newcomers

Rogers realizes it can be hard to start life in Canada without a solid credit score. That's why Rogers recognizes credit history from the following countries.

If you've moved within the past 2 years, here's a list of the types of documentation you can show, based on your previous country of residence:

- Australia: Driver's license, passport, Medicare card, immigration card

- Colombia: Colombian phone number, credit email address, citizenship card, immigration card

- India: Permanent account number, Aadhaar, passport, voter ID number

- Kenya: National ID number

- Mexico: Mexican address, Mexican credit card

- Nigeria: Bank verification number

- Philippines: Passport

- South Africa: Passport, South Africa ID

- South Korea: Resident Registration Number, Korean credit card, Korean phone number

- Spain: Passport

- Switzerland: Passport

- United Kingdom: UK address

- Ukraine: Passport, tax identification number, identity card

- United States of America: USA address

By bringing your credit score with you, it's easier to qualify for a credit card. Rogers also grants a credit limit of up to $20,000 to help you get started.

And, if you stop into a Rogers retail location, you can speak to someone in your native language since Rogers launched the "We Speak Your Language Program."

How to apply for a Rogers credit card

Applying for a Rogers credit card requires mostly the same steps as applying for any other credit card.

First, check your eligibility for the Rogers card you want. All cards require you to have reached the age of majority in your province.

Although there aren't income requirements for the basic Mastercard, the World Elite asks for $80,000 in personal or $150,000 household annual income, and the Legend asks for $150,000 in personal or $200,000 household annual income. On your credit card application, you'll need to list your income and your profession.

After you've filled out the rest of the application with your personal details, Rogers will do a credit check to find out your credit score. You'll need a score of at least 760 for any of these cards.

Here's what Rogers cardholders think

It's one thing to read about how we rated these Rogers credit cards, but we also like to look at what real cardholders have to say about using them. Rogers cards are reliable picks for people who already have a Rogers, Fido, Shaw, or Comwave service.

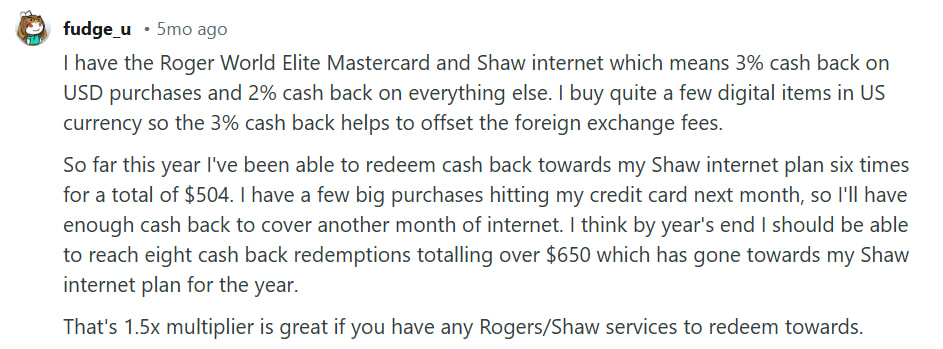

As this Redditor said, they've had no problems with redeeming their cash back and getting value from their Rogers card:

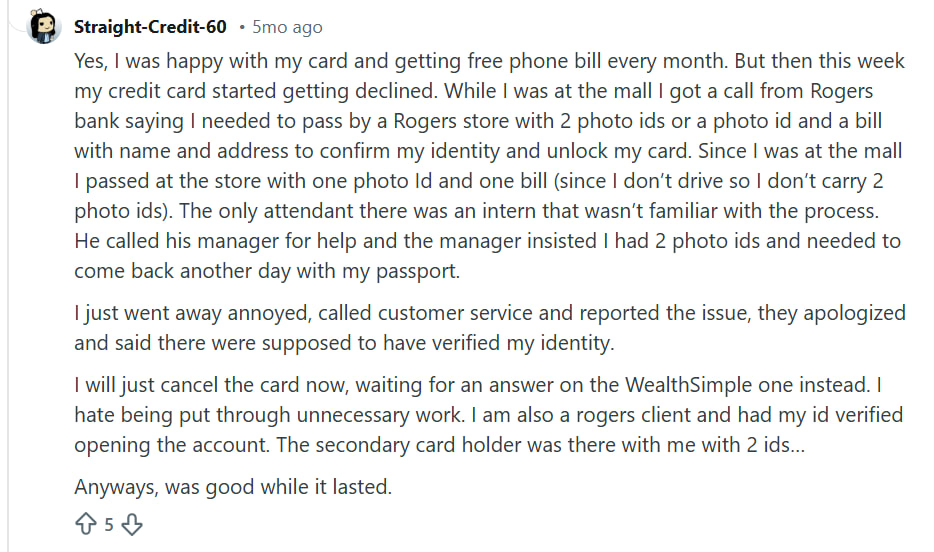

On the other hand, several Redditors pointed out problems with their cards being declined because they needed to verify their identities.

In one user's case, it was frustrating enough to make them cancel the card:

FAQ

Is there a Rogers credit card?

Yes, Rogers issues 3 credit cards: a basic no-fee card (the Rogers Red Mastercard), a no-fee World Elite Mastercard (the Rogers Red World Elite Mastercard), and its newest ultra-premium credit card, the World Legend Mastercard (Rogers Red World Legend Mastercard).

What are the best Rogers bank credit cards?

The Rogers Red World Elite Mastercard is the best Rogers bank credit card. It offers incredible value as a rare no-fee World Elite Mastercard. You'll get World Elite benefits without the usual cost. If you don't qualify for this card, the Rogers Red Mastercard is also a solid choice.

What are the disadvantages of Rogers Red World Elite Mastercard?

For a World Elite Mastercard, the insurance coverage could be more extensive. We love the fact that there's no annual fee, but the biggest drawback is the card's high income requirements: $80,000 in personal annual income or $150,000 in household annual income.

What are the perks of the Rogers Red World Elite Mastercard?

If you're a Fido, Rogers, Shaw, and Comwave customer, you'll get unlimited 2% cash back on all non-USD purchases, 3% back on USD purchases, and 5 Roam Like Home Days. There's also a 1.5x bonus when you redeem your cash back to pay for your Fido, Rogers, Shaw, and Comwave services.

Can I use my Rogers Mastercard at Costco?

Yes! The Rogers Red World Elite Mastercard is actually our top pick for the best credit card to use when shopping at Costco. If you're purchasing a warehouse haul at a U.S. location, you'll get 3% cash back. Canadian Costco purchases give you up to 2% back.

Editorial Disclaimer: The content here reflects the author's opinion alone. No bank, credit card issuer, rewards program, or other entity has reviewed, approved, or endorsed this content. For complete and updated product information please visit the product issuer's website. Our credit card scores and rankings are based on our Rating Methodology that takes into account 126+ features for each of 251 Canadian credit cards.